What to Do With Your Money After Becoming Debt-Free

Surmount Blogs

Just paid off debt? Learn exactly what to do with money after debt free—save, invest, and grow wealth smartly.

What to Do With Your Money After Becoming Debt-Free

You're Debt-Free — Now What?

Paying off the last of your debt is a milestone worth celebrating. But once the relief settles, a new question takes over: what to do with money after debt free? For years, every extra dollar had a job — a loan, a balance, a payment plan. Now that job is gone, and the freedom can feel disorienting.

The good news is that this is one of the best financial positions to be in. With no debt pulling at your paycheck, you have room to build real wealth. The key is turning that freedom into a plan before lifestyle creep or decision paralysis eats into your progress.

First Steps to Investing With No Debt

Before diving into the markets, a few foundational moves make everything else work better. These are the first steps to investing with no debt that most financial experts agree on:

Confirm your emergency fund is fully funded

Open the right tax-advantaged accounts

Decide how much goes toward retirement vs. flexible investing

Set up automatic contributions so you don't have to think about it every month

How Much to Keep in an Emergency Fund

A common mistake once debt is gone is redirecting everything into investments. Don't — a fully funded safety net is still one of the five pillars of financial security every investor should have in place first. Most planners recommend keeping 3–6 months of essential expenses in a high-yield savings account before investing aggressively, a range consistent with guidance from sources like Vanguard's emergency fund research.

If your expenses run around $3,000–3,500 a month, that means a cushion of roughly $10,000–$21,000. This isn't wasted money — it's what keeps you from having to sell investments (or go back into debt) the next time your car breaks down or you face a job loss.

Roth IRA vs. Brokerage Account: Which Comes First?

Once your safety net is in place, the next debate is usually Roth IRA vs. brokerage account. Here's a simple way to think about it (rules on contributions and withdrawals are laid out clearly by the IRS):

Roth IRA — Best for retirement savings; contributions grow tax-free, and you can withdraw your original contributions penalty-free if needed

Taxable brokerage account — Best for flexible goals like a home down payment or early retirement, since there are no withdrawal restrictions

401(k) match — Always contribute enough to get your full employer match first — it's an immediate, guaranteed return

For most people newly free of debt, the order looks like: capture the 401(k) match → max out the Roth IRA → then build a taxable brokerage account with any leftover surplus.

What to Do With Extra Money Each Month

Once your accounts are set up, the real question becomes ongoing: what to do with extra money each month, month after month. One of the simplest ways to answer that consistently is to automate your dollar-cost averaging so contributions happen on schedule, not on willpower. A simple system might look like:

Automate a fixed percentage into your 401(k)

Automate a monthly Roth IRA contribution (even $200–300 adds up)

Send remaining surplus to a taxable brokerage account

Review and rebalance quarterly — not daily

The goal isn't to make perfect decisions every month. It's to make good decisions automatically, so willpower is never the deciding factor.

Why You Should Automate Your Investments

Here's the uncomfortable truth: most people don't fail at investing because they pick bad assets — they fail because they stop being consistent. Life gets busy. Motivation fades. A single missed contribution turns into six.

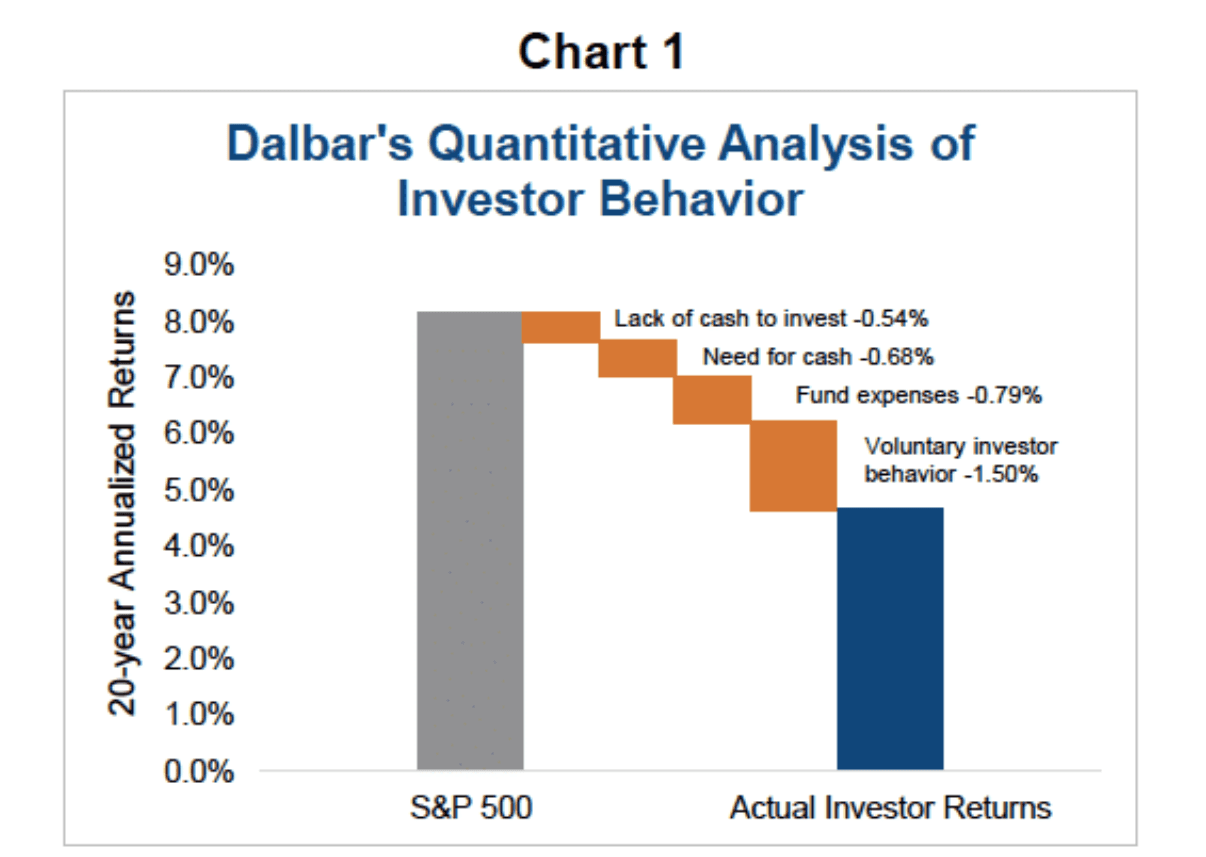

This is why so many experienced investors automate their investments — it's one of the most effective ways to sidestep the hidden dangers of emotional investing that quietly erode long-term returns. Research from DALBAR's investor behavior studies consistently shows that emotional, poorly timed decisions — not bad asset selection — are the biggest drag on long-term returns.

Investing Without Picking Stocks

Not everyone wants to spend hours researching individual companies — and you don't have to. If you're unfamiliar with how this works in practice, this guide to automated investing strategies breaks down the main approaches available today. Investing without picking stocks through diversified index funds or rules-based strategies can outperform many individual stock-pickers over time, a pattern well documented in CFA Institute research on active vs. passive investing, largely because it removes emotional decision-making from the equation.

Instead of asking "which stock should I buy this month?", the better question becomes: "what system will keep me investing correctly, automatically, for the next 10 years?"

Building a Set-and-Forget Investing Strategy

This is really the end goal for anyone newly debt-free: a set-and-forget investing strategy that runs quietly in the background. If you're evaluating whether a platform like Surmount fits that role, our 2026 review breaks down exactly what it does well — and where it doesn't.

A good long-term system should:

Require minimal day-to-day management

Rebalance based on rules, not emotions

Scale automatically as your income grows

Reduce the temptation to time the market or chase headlines

Debt freedom gives you the capacity to invest. A systematic, automated approach gives you the structure to actually follow through — which, over 10, 20, or 30 years, tends to matter far more than any single stock pick ever will.

Turn Your Debt-Free Fresh Start Into a Systematic Wealth Plan

Getting out of debt was the hard part. Now the challenge shifts from discipline to consistency — and that's exactly where most people, even well-intentioned ones, quietly fall off track.

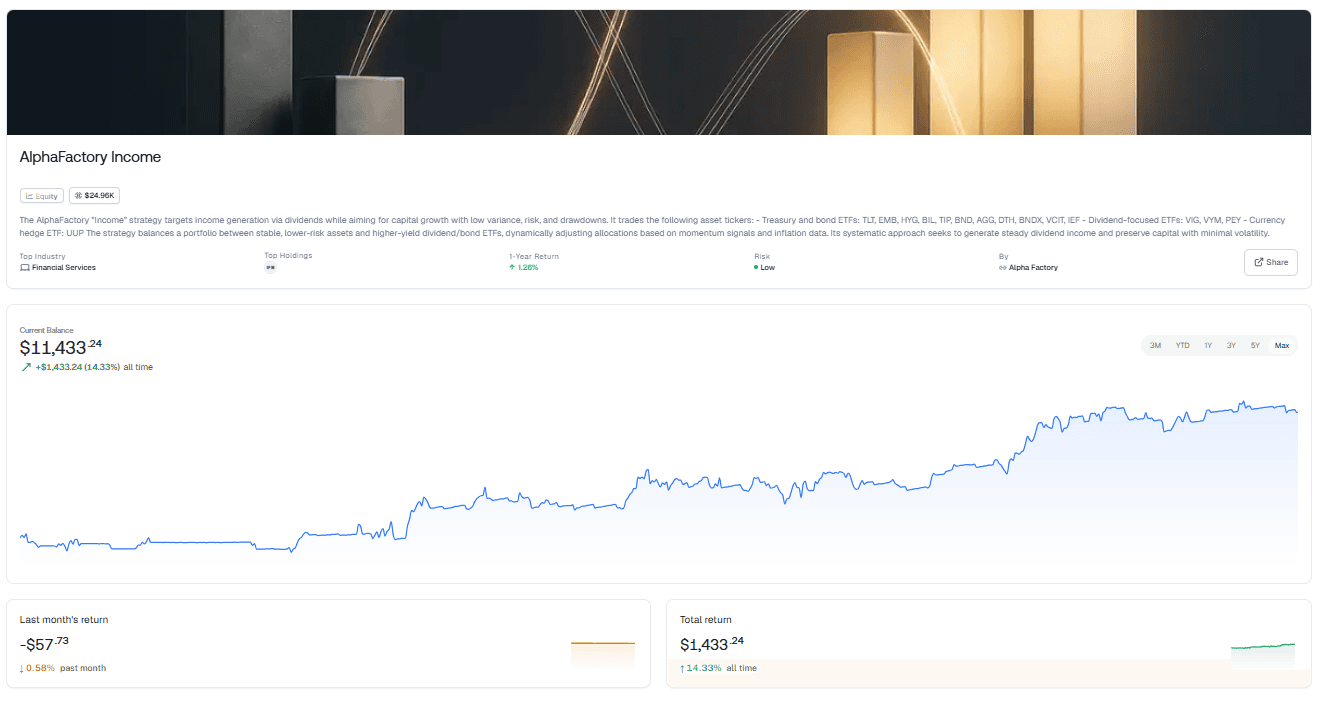

The AlphaFactory Income strategy on Surmount was built for exactly this stage of an investor's journey. It combines dividend-focused ETFs (like VIG and VYM) with treasury and bond ETFs (like TLT and BND), dynamically adjusted based on momentum signals and inflation data — all with one goal: steady income and capital preservation, without the emotional guesswork.

Here's why it fits so well right now:

Built for stability, not speculation — the strategy targets low variance and minimal drawdowns, ideal for someone building their first real investment foundation

Diversified from day one — blends income-generating dividend stocks with lower-risk bond exposure, so you're never overly exposed to a single asset class

Fully automated rebalancing — no need to check charts or make monthly decisions; the system adjusts allocations as market conditions shift

Removes the discipline problem entirely — the same automation that keeps your 401(k) and Roth contributions consistent now extends to your entire income-focused portfolio

No coding, no complexity — connect your existing brokerage account and deploy the strategy in minutes

You already did the hardest part — becoming debt-free. Don't let the next chapter stall out on indecision or inconsistency.

Deploy the AlphaFactory Income Strategy on Surmount →

Frequently Asked Questions

What should I do with my money after becoming debt free?

Start by confirming your emergency fund is fully funded, then prioritize your 401(k) match, a Roth IRA, and a taxable brokerage account in that order.

How much should I keep in savings before investing?

Most experts recommend 3–6 months of essential expenses in a high-yield savings account before directing extra money toward investing.

Is a Roth IRA or brokerage account better after paying off debt?

A Roth IRA is best for long-term retirement savings, while a brokerage account offers more flexibility for goals like a home down payment or early retirement.

How do I stay consistent with investing every month?

Automating your contributions removes the need for willpower and helps you invest consistently, even when life gets busy.

Why should I consider automated investing instead of picking stocks myself?

Automated, rules-based strategies remove emotional decision-making and help ensure consistent execution — something that's difficult to maintain manually over time.

Automate any portfolio using data-driven strategies made by top creators & professional investors. Turn any investment idea into an automated, testable, and sharable strategy.