REITs vs. Rental Properties: A Practical Guide for Smarter Returns

Surmount Blogs

REITs vs. Rental Properties: A guide to why institutional scale and tax efficiency often beat DIY landlording. Learn to trade "tangibility bias" for liquid, high-velocity compounding.

REITs vs. Rental Properties: A Practical Guide for Smarter Returns

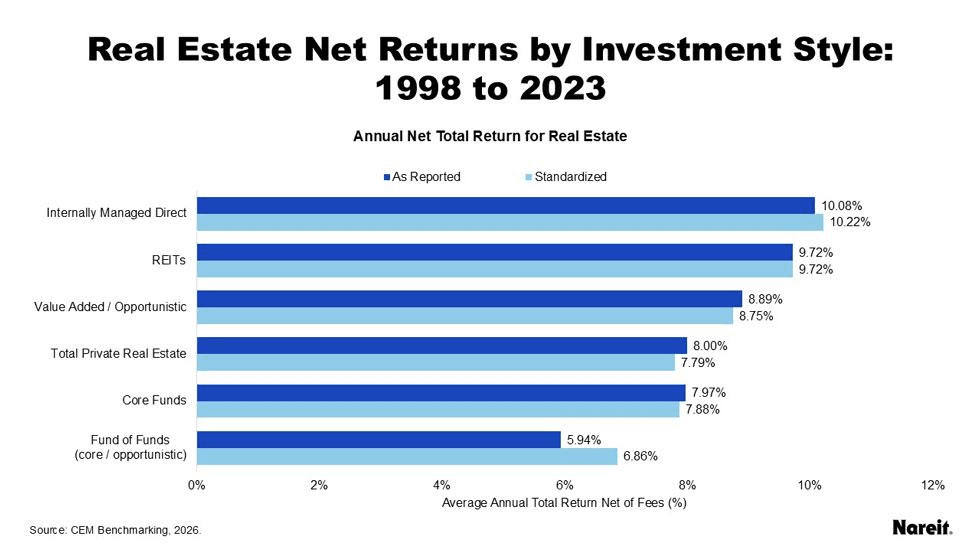

Comprehensive long-term data indicates that Public REITs typically outperform private real estate (such as rental properties) on a net total return basis. For instance, according to a prominent 2024-2026 CEM Benchmarking study covering a 26-year period (1998–2023), listed equity REITs produced an average annual net return of 9.72%, while private real estate returned 7.79%.

This nearly 200-basis point delta may seem marginal to the uninitiated, but over a twenty-year horizon, the power of geometric compounding renders the difference astronomical.

The disparity arises because the real estate investor is often blinded by the "tangibility bias"—the psychological comfort of touching brick and mortar. However, sophisticated capital treats real estate as a cash-flow engine, not a hobby. When you strip away the romanticism of property ownership, you understand that private rentals are often burdened by "leakage"—unseen costs in the form of maintenance cap-ex, localized economic volatility, and the massive opportunity cost of your own time.

To invest like an institutional strategist, one must move beyond the "landlord" archetype. By the end of this analysis, we will deconstruct the mechanisms of REITs—from their superior liquidity profiles to their tax-advantaged structures—to show you how to capture real estate alpha without the anchor of physical management. You are about to see the horizon through a professional lens, spotting the inefficiencies that the DIY market consistently fails to price in.

The Calculus of Returns and Risk

To the layperson, a physical deed might feel like "real" wealth that is immune from being devalued. However, to institutional-grade investors, the "tangibility" of a single-family rental is often a deceptive veil for systemic inefficiency.

True outperformance is a function of structural alpha—the inherent advantages built into the vehicle itself rather than the underlying dirt. Here is why the mathematical gravity of REITs consistently pulls ahead of the DIY landlord.

1. The Economies of Scale (The "Wholesale" Advantage)

A retail investor buying a rental property pays retail prices: for the mortgage, the maintenance, and the management. Conversely, a REIT operates at an institutional scale that collapses these costs. When a REIT manages 50,000 apartment units, their cost per square foot for a roof replacement or insurance premium is a fraction of what you would pay for a single duplex. This spread between retail and institutional operating costs directly pads the bottom line of the REIT shareholder.

2. Diversification vs. Idiosyncratic Risk

In private real estate, you are exposed to idiosyncratic risk: a single bad tenant, a localized rezoning shift, or a specific pipe burst can vaporize an entire year’s yield. REITs mitigate this through radical diversification across geographies and asset classes (such as cell towers, cold storage, or data centers) that are inaccessible to the individual.

3. The Reinvestment Velocity

Most rental property owners "bleed" their cash flow on small, recurring expenses or let it sit in a low-interest savings account for the next "emergency repair." REITs, however, utilize a sophisticated internal rate of return (IRR) model. They take the massive cash flows generated by the portfolio and immediately redeploy them into new acquisitions or development projects. This constant velocity of capital creates a compounding effect that a stagnant, single-unit rental simply cannot match.

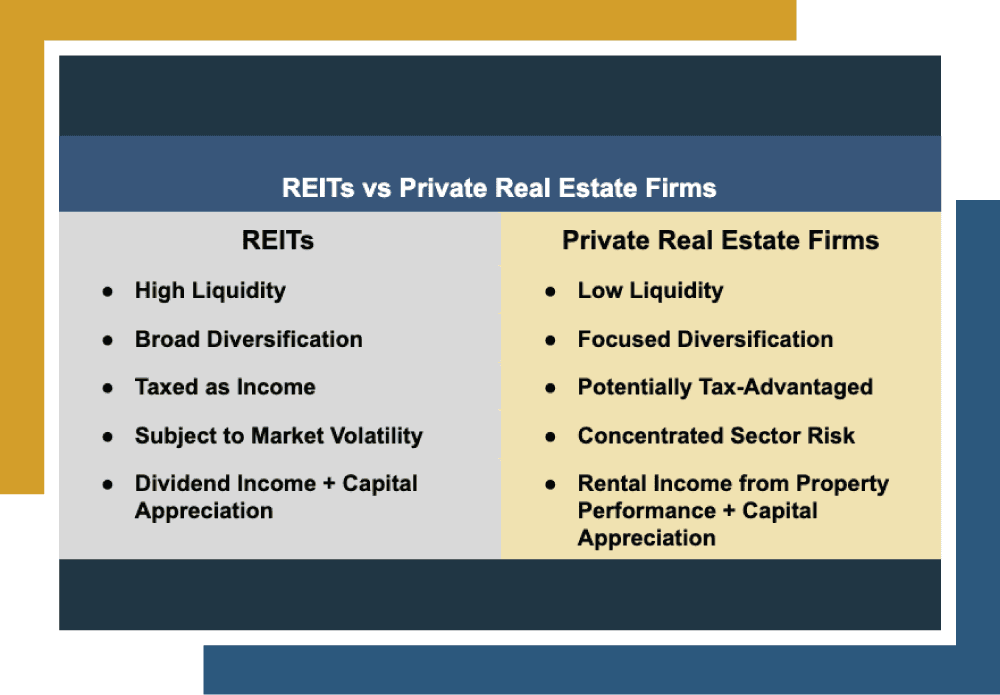

4. Liquidity as a Risk-Mitigant

The ability to exit a position in milliseconds is not just a convenience; it is a financial superpower. If a specific real estate sector (like B-class office space) faces a structural decline, a REIT investor can reallocate their capital to Industrial Logistics instantly. The private landlord, meanwhile, is tethered to a sinking ship by a six-month closing process and heavy transaction costs.

Always remember that you aren't just choosing an asset; you are choosing an operating system. REITs run on a high-speed, institutional OS, while private rentals often run on manual, high-friction legacy code.

Structural Alpha of REITs over Rentals: Leverage, Taxes, and Human Capital

High-return investing is rarely about the asset class in a vacuum; it is about the structural environment that houses the asset. This is why sophisticated allocators focuse on the efficiency of the vehicle from a structural perspective:

1. The Leverage Paradox: Institutional vs. Personal Liability

The DIY landlord typically utilizes a recourse mortgage, meaning their personal credit and global assets are on the line if the investment soured. Conversely, REITs employ corporate-level, non-recourse debt.

By investing in a REIT, you benefit from "scale-enhanced leverage." These entities access debt markets—such as unsecured bonds—at rates a retail borrower could never touch. They amplify returns through institutional creditworthiness without requiring you to sign a personal guarantee. You gain the upside of debt with a "firewall" protecting your personal balance sheet.

2. The Tax Shield: Eliminating Double Taxation

In the realm of private corporations, profits are taxed at the entity level and again at the individual level (dividends). REITs are a legal anomaly designed for efficiency: provided they distribute at least 90% of their taxable income to shareholders, they pay zero corporate-level income tax.

This allows capital to flow from the tenant's rent check to your brokerage account with fewer "toll booths" along the way. Furthermore, a portion of REIT distributions is often classified as "Return of Capital," which isn't taxed in the current year but instead lowers your cost basis, effectively deferring your tax liability until you sell.

3. Protecting Your Human Capital: The Opportunity Cost of "Sweat"

Your most valuable asset isn't a duplex; it is your future earning power. Every hour spent vetting a tenant, managing a contractor, or auditing a property manager is an hour stolen from your primary career or high-level ventures.

Private Real Estate: Essentially a part-time job with high overhead and low scalability.

REITs: Pure capital appreciation that scales infinitely without a single minute of your labor.

Smart investing is not just about the gross return; it’s about the net-net return after accounting for taxes, risk-adjusted leverage, and the depletion of your own time.

Investing Like An Allocator, Not A Landlord

If you’ve followed the logic of this guide, you’ve realized that the optimal approach to real estate isn't about owning the most bricks; it’s about owning the most efficient cash flows. While the DIY landlord is busy negotiating with a plumber, the institutional-grade investor is busy optimizing their Sharpe Ratio.

But how does one bridge the gap between understanding this theory and executing it across a global landscape?

Well, one way to approach that with precision is through a systematized approach that treats real estate as a factor-based equity investment rather than a hobby. This is the "Smart Money" transition in its purest form.

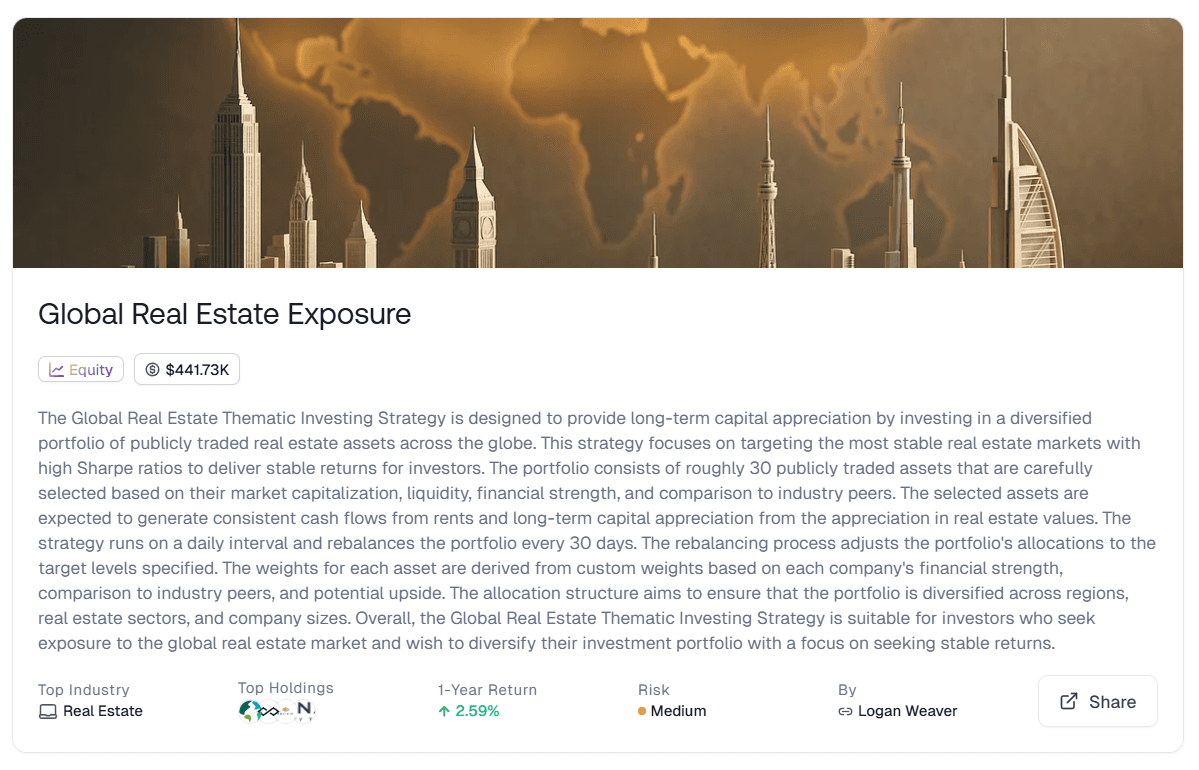

This is best manifested in the The Global Real Estate Thematic Investing Strategy

Why This Strategy Outperforms the "Hobbyist" Model:

Algorithmic Precision: The strategy filters a global universe for roughly 30 publicly traded assets, selected specifically for financial strength, liquidity, and peer-to-peer alpha.

The 30-Day Rebalancing Edge: Most investors suffer from "Endowment Effect"—holding underperforming physical assets because the friction to sell is too high. Our strategy rebalances every 30 days, mathematically stripping emotion out of the equation to maintain optimal weights.

Global Diversification (The "Free Lunch"): By diversifying across regions and specialized sectors (Data Centers, Logistics, Medical Labs), we mitigate the "single-point-of-failure" risk inherent in a local rental market.

Institutional Leverage: We only target companies with the balance sheet scale to utilize non-recourse debt, protecting your personal liability while amplifying your returns.

Stop Managing Liabilities. Start Allocating Capital.

The difference between a 4% and an 8% annual return over 20 years is the difference between a comfortable retirement and generational wealth. Don't let the "romance" of physical deed ownership anchor your net worth to an inefficient asset.

Are you ready to stop being a landlord and start being an allocator? [Click here to explore the Global Real Estate Thematic Investing Strategy and see how our automated data-driven approach can elevate your portfolio today.]

Automate any portfolio using data-driven strategies made by top creators & professional investors. Turn any investment idea into an automated, testable, and sharable strategy.