Invest Like Peter Lynch: The “Boring Business” Strategy That Built a Fortune

Surmount Blogs

Discover how Peter Lynch’s timeless “boring business” approach can help investors escape market hype and build long-term wealth. Learn to focus on resilient, undervalued companies for steady growth.

Invest Like Peter Lynch: The “Boring Business” Strategy That Built a Fortune

Peter Lynch is considered by many among the absolute greats of the investing space.

He is widely considered the "Ultimate Stock Picker" and a pioneer of the strategy of Growth at a Reasonable Price (GARP). His legacy is built on the fact that he didn't just beat the market; he crushed it. During his 13-year tenure at the Fidelity Magellan Fund, he averaged a 29.2% annual return, nearly doubling the S&P 500's performance over that same span.

Today, in the modern stock market dynamics we are faced with investing has become increasingly volatile, complex, and crowded. Many investors feel like they are competing against supercomputers in a game they can't win. Afterall, there are simply too many variables to simultaneously keep track of, including (but not limited to) tariff shocks, geopolitical uncertainties, and the potential of a vicious AI bubble collapse.

In times like this, turning to Lynch’s "One Up on Wall Street" philosophy offers a grounded alternative.

Escaping Concentration Risk

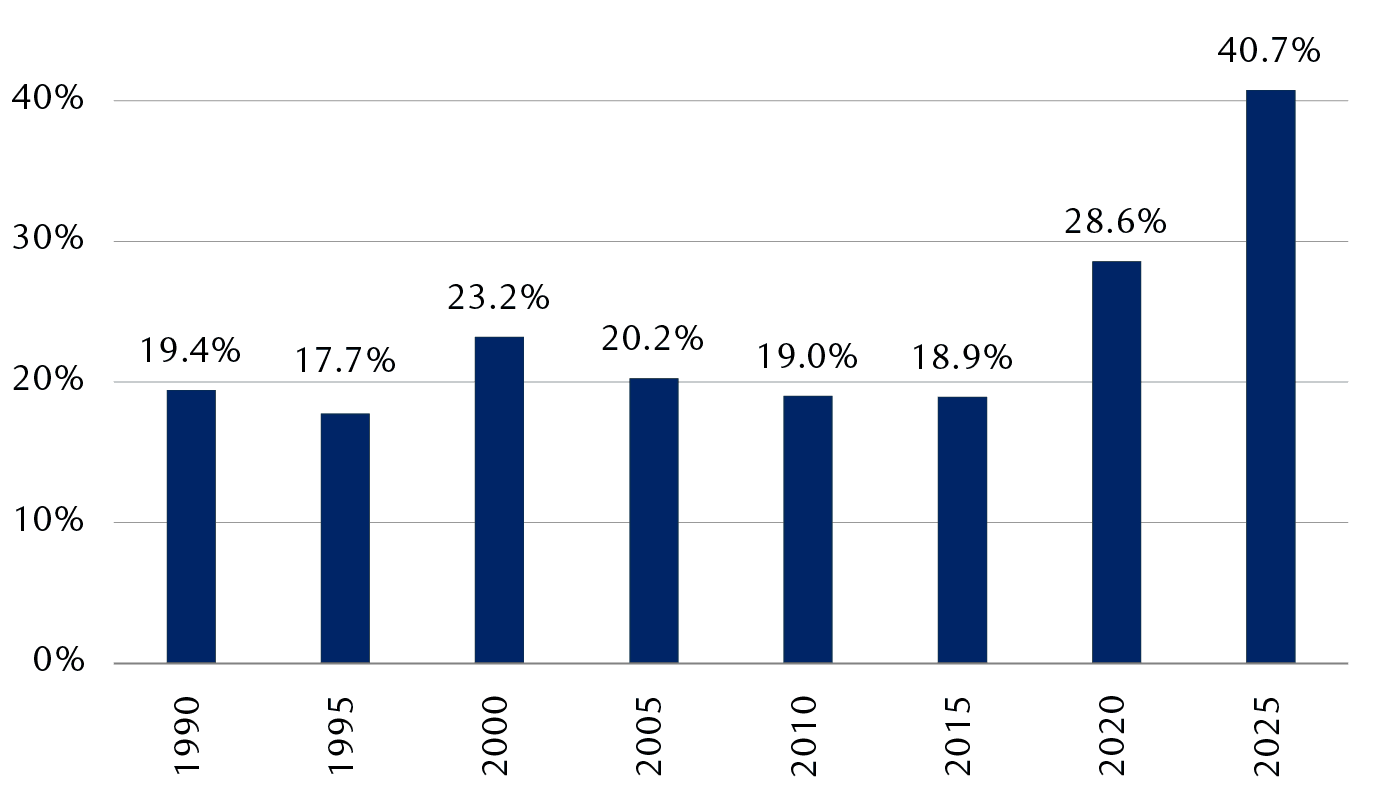

RBC Wealth Management recently pointed out that, at the beginning of this year, the 10 largest companies in the S&P 500 accounted for nearly 41% of the index’s total weight.

Looking at this figure across the last 35 years, we come to see that level of concentration is a historic outlier, more than doubling the 19% weighting seen just a decade ago.

For an investor today, this "Great Narrowing" understandably creates a very precarious environment. While the S&P 500 appears diversified, it has effectively become a directional bet on just a single theme, which is AI and Big Tech.

Now, Peter Lynch absolutely loathed the idea of being a "closet indexer" or following the herd into "hot" sectors. He has, in his writings, referred to institutional investors as a "blundering herd" that often moves together, overlooks obvious information, and repeats predictable errors.

As such, his approach offers a structural escape from today’s concentration risks through three specific disciplines:

The "Boring" Business Buffer

Lynch famously sought out companies that sounded dull or even slightly repulsive to Wall Street. He argued that a company that "processes sewage" or "makes bottle caps" was less likely to be bid up to the irrational P/E multiples we see in today's top 10.

While the Mag 7 is almost entirely tied up to the complex, high-stakes evolution of AI, a Lynch-style portfolio would be anchored in businesses whose success depends on simple, predictable human needs.

Earnings-to-Growth Alignment

The data shows a widening gap where the top 10 companies on the S&P 500 only represent 41% of weight but only 32% of earnings. Lynch would view this as a red flag for "diworsification."

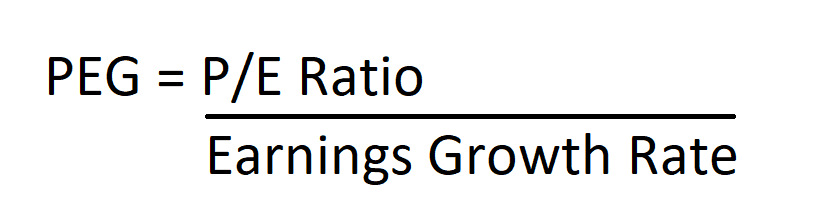

His North Star, of course, was the PEG Ratio:

Relying on the PEG ratio

This helps investors by providing a growth-adjusted valuation that distinguishes between stocks that are "expensive for a reason" and those that are simply overvalued.

So if a Megacap’s valuation has outrun its fundamental profitability, Lynch’s math simply wouldn't allow him to buy it—forcing him instead toward the "Equal Weight" opportunities where value still exists.

Avoiding "Idiosyncratic Shock"

One consistent mental model seen throughout Peter Lynch’s writings is how he thinkgs in life cycles, rather than the typical sector divisions. In his book “One Up on Wall Street”, Peter Lynch categorizes stocks into six distinct types:

Slow Growers,

Stalwarts,

Fast Growers,

Cyclicals,

Turnarounds, and

Asset Plays

These categories allow investors to differentiate between stable, mature companies and high-risk, high-reward opportunities. This is also relevant in the modern context where a single supply chain hiccup in Taiwan or a shift in AI regulation in Europe can devastate a passive portfolio.

Company Facts Beat Macro Forecasts

Peter Lynch has famously stated that “if you spend 13 minutes a year on economics, you’ve wasted 10 minutes.” This, slightly sarcastic line actually sums up his philosophy pertaining macro noise.

In a 2026 market obsessed with Fed meeting transcripts and global GDP forecasts, Lynch’s indifference to the "big picture" is his greatest, albeit most peculiar, edge. In order to structurally achieve this, however, one must focus on a few key areas:

The "Company-Specific" Shield

If you pick a company with a dominant local position, a great balance sheet, and a product people can’t live without, it doesn't matter what the Chairman of the Federal Reserve says. That company will return value to its shareholders.

Now while that might sound overly simplistic, the logic is actually sound. Interest rates might rise, but if a company is the low-cost provider of trash collection or heart valves, people will still pay.

So while the S&P 500 swings 2% based on a single inflation print, a Lynch-style investor is looking at whether a specific retailer just improved its inventory turnover. One is a guess on the economy; the other is a fact about a business.

Market Timing is a "Fool’s Errand"

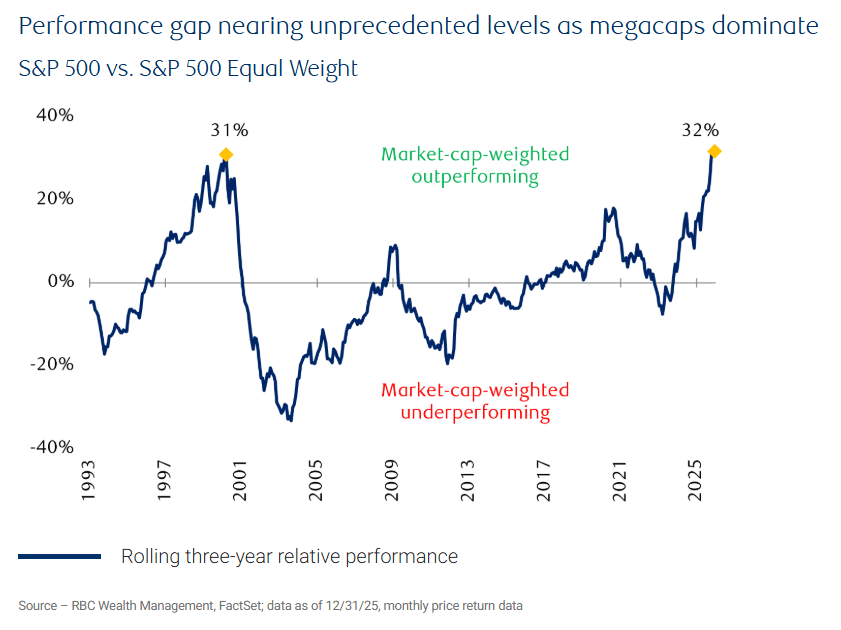

The graph above highlights that the S&P 500 Equal Weight has trailed the Cap-Weighted index by 32% over three years. This means that the average company in the index has been left in the dust by a handful of mega-cap giants.

To a Lynch-style investor, this isn't a reason to panic at all.

In fact, Peter Lynch never tried to predict when the "rotation" would happen. He simply bought the undervalued companies and waited. The idea here is that the "big money" isn't in the first 10% move, but in the multi-year compounding.

If you jump in and out of the market to avoid a "macro dip," you risk missing the two or three best days of the year that account for most of the gains.

Now of course, this by no means is a call to ignore macroeconomic data. However, it simply means a blind reliance on forecasts coming from “ivory towers” must hold little weight over "boots on the ground" data.

So to put it simply, following the Lynch investing style wouldn't care about the national unemployment rate as much as it would whether the local Hilton is fully booked or if the nearby Ford dealership has a 6-month backlog. This is because these are leading indicators. By the time the "Macro Noise" confirms a recession or a recovery, Lynch’s "Quiet Facts" have already told us the story months in advance.

Applying The Lynch Approach With Smart Strategies

Practically, in 2026, a Peter Lynch-inspired strategy must intrinsically be anti-cyclical. That means finding opportunities that thrive even when headlines scream doom or when the market swings wildly.

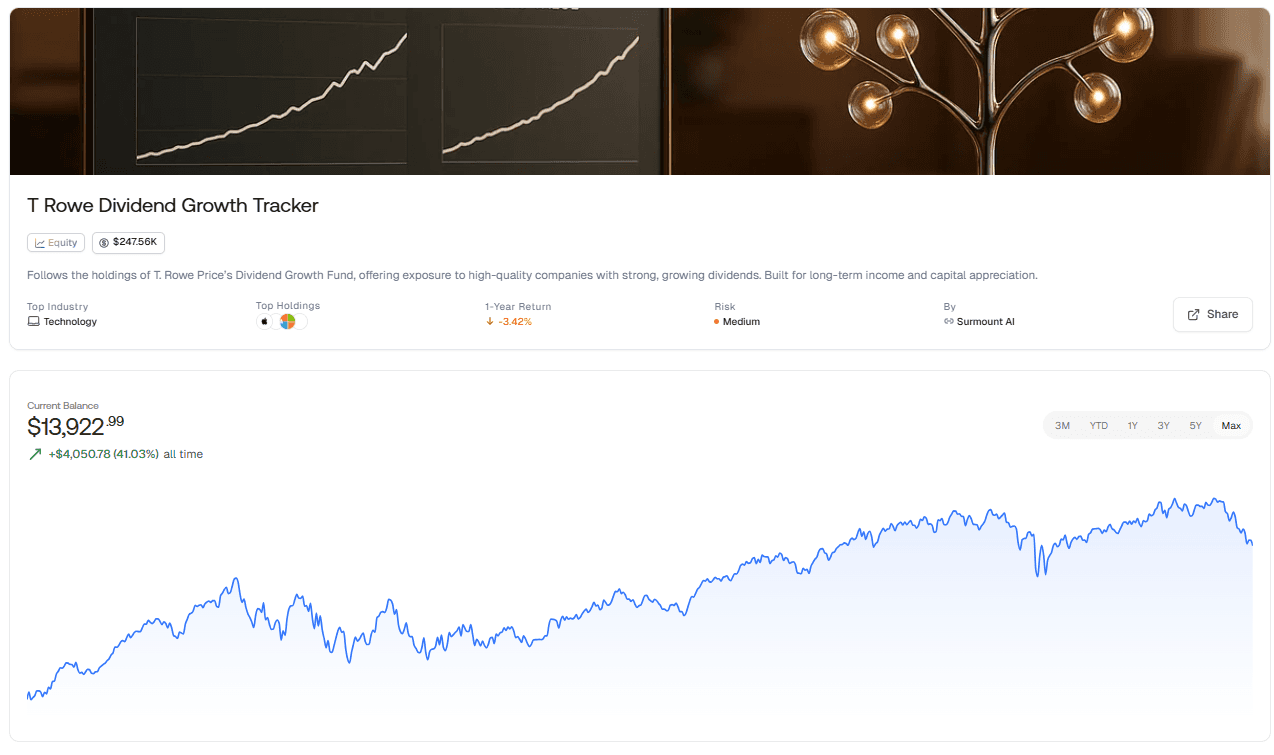

One way investors could actually implement this is through Surmount’s T. Rowe Price Dividend Growth Fund.

By focusing on high-quality, dividend-growing companies, it anchors your portfolio in businesses with stable earnings, resilient balance sheets, and products people can’t live without—exactly the kind of “boring” yet essential companies Lynch loved.

This approach doesn’t chase fads or trendy sectors; it lets you sidestep the hype-driven volatility that dominates today’s mega-cap and AI-heavy markets. Meanwhile, reinvested dividends become a quiet compounding engine, steadily building wealth while others worry about timing the next market move.

In essence, this strategy is a shield and a growth engine in one: it protects your capital during turbulent cycles while positioning you to capture reliable, long-term appreciation. For investors seeking a Lynch-style edge in 2026, it’s not just smart—it’s almost irresistible.

Automate any portfolio using data-driven strategies made by top creators & professional investors. Turn any investment idea into an automated, testable, and sharable strategy.