Why Credit Markets Always Crack Before Stocks Do

Surmount Blogs

Credit markets often reveal financial stress before stocks react. Learn how widening credit spreads, liquidity pressures, and fund redemptions can signal the next major equity downturn.

Why Credit Markets Always Crack Before Stocks Do

The market has been a bit of a wild ride lately, swinging between "panic mode" and "recovery" with serious whiplash, owing to shifting geopolitical tensions in the Middle East and resultant fluctuations in oil prices. While indices faced sharp declines last week, they staged a major comeback on Monday and Tuesday.

Investors might be tempted to view these swings as simple noise or technical corrections. Check your portfolio, see the green, and breathe a sigh of relief. Of course, this is what most market participants are doing right now, and understandably so.

But one area very few equity investors are scrutinizing—yet one that holds the blueprint for the next major market move—is the credit market. While stocks have the potential to trade heavily on sentiment and multiples, the credit market trades on the cold, hard reality of solvency.

Recently, credit markets have been flashing warning signs with significant stress appearing in the private credit sector and a notable "flight to quality" in government bonds. Major firms like BlackRock and Blackstone have recently capped withdrawals from flagship credit funds after investor redemption requests surged beyond limits. Similarly, following warnings from JPMorgan CEO Jamie Dimon about hidden risks, the recent bankruptcy of firms like Thrasio has fueled fears of a broader systemic "washout" in private lending.

If you are an investor, you have two choices: continue to look through the windshield at the flashing lights of the stock market, or start checking the engine oil pressure in the credit markets. History has consistently shown that the equity market is a theater of sentiment, but the credit market is the theater of necessity. When liquidity dries up in the credit markets, it acts as the primary transmission mechanism for systemic failure, inevitably spilling over into the equity indices.

The Seniority Advantage: Why Credit Markets Are the "Canary in the Coal Mine"

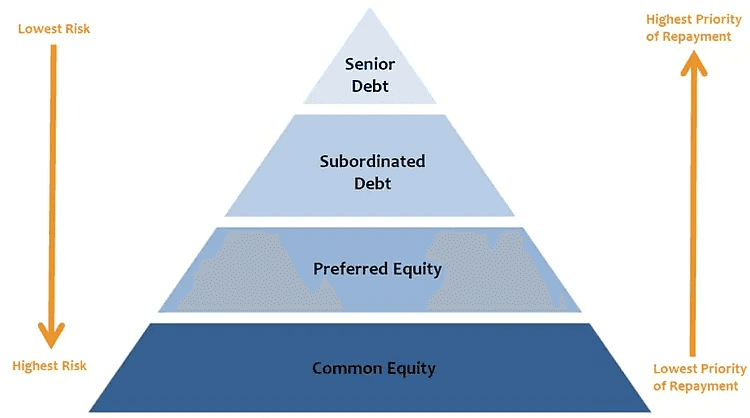

To understand why equity markets are often the last to acknowledge a structural shift, we must first understand the fundamental divide in the capital structure. In any corporate entity, the capital stack is governed by the absolute priority rule: in the event of distress or liquidation, debt holders are paid in full before a single cent is distributed to equity holders.

Because credit investors—lenders, bondholders, and commercial banks—stand higher in this hierarchy, their relationship with risk is inherently different from that of an equity shareholder. An equity investor is effectively long volatility and "delta," seeking exponential upside from growth, multiple expansion, and dividends. Conversely, a credit investor is effectively short volatility; their primary objective is the preservation of principal and the collection of a fixed coupon.

When a company faces headwinds, an equity investor might view a dip in share price as a "buying opportunity" or a "temporary correction." The credit investor, bound by restrictive covenants and a limited upside, views the exact same data through the lens of default risk. They do not care about the "dream" of future earnings; they care about the Interest Coverage Ratio and the Net Debt to EBITDA multiple.

Why Spreads Speak Louder Than Prices

The most powerful tool in the credit investor’s arsenal is the credit spread—the additional yield an investor demands for holding a corporate bond over a risk-free government bond (like a Treasury).

When these spreads begin to widen, it is the market’s way of saying that the cost of capital is increasing, often because the perceived risk of default has surged. This widening is the "canary in the coal mine" for three specific reasons:

Refinancing Pressure: Most corporations operate on a cycle of rolling over their debt. When credit spreads spike, the cost to refinance maturing debt becomes prohibitive. If a company can no longer roll over its debt at a sustainable rate, the "liquidity crisis" quickly evolves into a "solvency crisis."

Covenant Tightening: As credit conditions deteriorate, lenders become more draconian with covenants. These restrictions often force companies to slash capital expenditures (CapEx) or dividends to preserve cash—actions that directly erode the growth narrative that keeps equity prices elevated.

The Information Lag: Equity markets are driven by sentiment, analyst upgrades, and retail participation, all of which are prone to cognitive bias. Credit markets, dominated by institutional players, complex modeling, and rigorous due diligence, are far more clinical. When credit investors signal distress, they are reacting to fundamental cracks in the balance sheet that retail equity investors simply cannot see until the quarterly earnings release confirms the disaster.

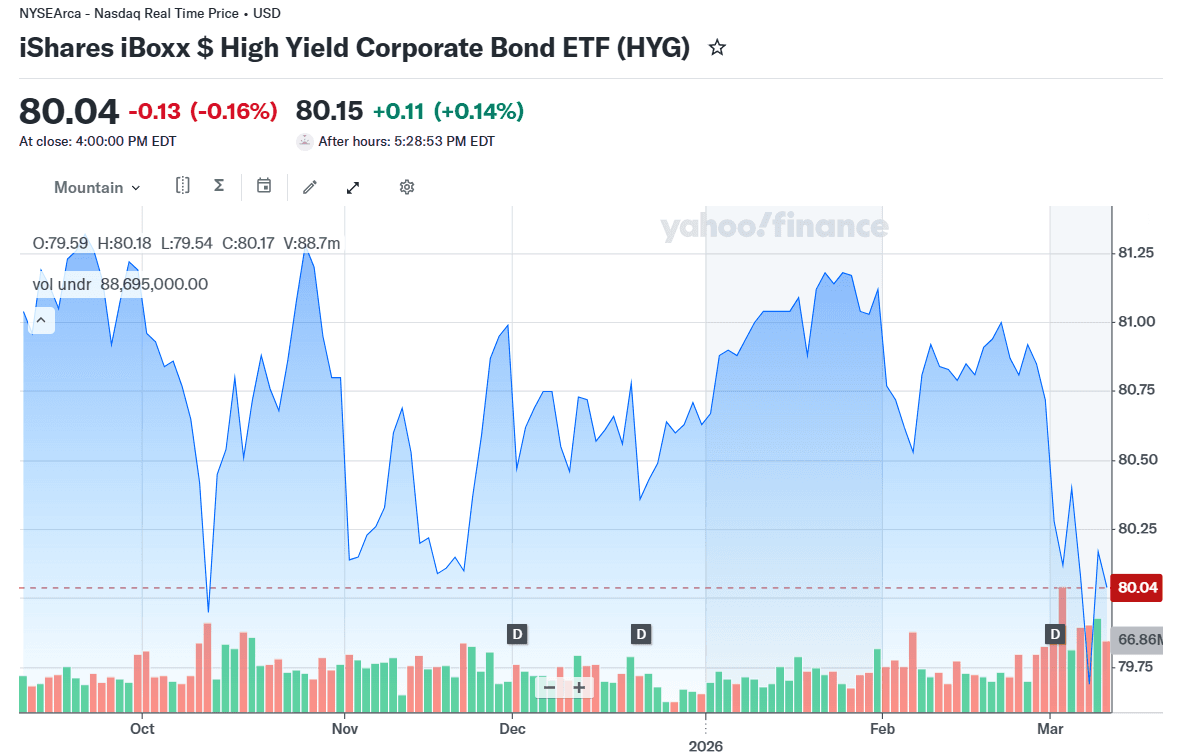

In short, when you see high-yield bonds selling off, as seems to be the case with the iShares iBoxx High Yield Corporate Bond ETF (HYG), it could potentially signal a divergence between the "hopes" of the equity market and the "realities" of the credit market. Smart investors recognize that the credit market is not just predicting the future; it is the mechanism that eventually forces the equity market to catch up to the truth.

The Liquidity Trap: How Fund Redemptions Force Asset Sales

Equity investors often perceive market crashes as discrete events triggered by "bad news"—a missed earnings report, a geopolitical shock, or a sudden regulatory change. However, beneath the surface of these headline-grabbing events often lies a mechanical, reflexive process: the liquidity trap of forced deleveraging.

The Mechanism of Forced Deleveraging

Credit markets function on the promise of liquidity. When investors are confident, they park capital in credit funds, expecting to be able to withdraw those funds at par value whenever they choose. However, credit instruments—especially high-yield bonds and private credit—are inherently less liquid than the large-cap stocks that make up major equity indices.

When market sentiment sours, investors begin requesting redemptions from credit funds. To honor these requests, fund managers must raise cash. Under normal conditions, they would sell the bonds they hold. But when a broader credit shock occurs, the market for those bonds evaporates—there are no buyers, or buyers are only offering "fire-sale" prices.

The "Liquidate What You Can, Not What You Want" Rule

This is the moment where the contagion spreads to the equity market. Because fund managers cannot sell their illiquid, distressed bonds without taking catastrophic losses, they are forced to sell their most liquid assets to meet redemption obligations.

Fund managers often hold a "liquidity bucket" of blue-chip, highly liquid equities alongside their credit positions. When the credit side of their portfolio freezes, these blue-chip stocks become the "ATM" for the fund.

It is important to note that even if a company’s fundamentals are strong, the sudden, massive selling pressure from funds desperate to raise cash causes its stock price to collapse. This creates a reflexive feedback loop: as stock prices fall, margin calls are triggered for other market participants, leading to further forced selling.

Why Monitoring Redemptions Matters

For the equity investor, ignoring credit fund flows is akin to ignoring the tide going out before a tsunami. By tracking data such as monthly redemption trends in high-yield bond ETFs or shifts in institutional credit fund flows, you can gain a "early warning" signal.

When you see credit funds experiencing net outflows while spreads are simultaneously widening, the risk of a "liquidity-driven" equity drawdown rises significantly. The equity market is not crashing because the companies themselves are failing; it is crashing because the financial plumbing is being forced to flush its most liquid assets to stay solvent.

Recognizing this distinction allows you to identify when market volatility is driven by structural mechanics rather than fundamental business decline—a crucial edge for protecting capital during systemic liquidity crunches.

Liquidity Signals: Reading the "Temperature" of the Market

In the complex machinery of global finance, liquidity is the lubricant that allows assets to move from buyers to sellers without causing violent price swings. When this lubricant dries up, market "friction" increases, leading to the rapid, cascading sell-offs that characterize equity crashes. For the observant investor, the "temperature" of the market is rarely found in the P/E ratios of the S&P 500, but rather in the plumbing of the credit markets.

1. High-Yield (Junk) Credit Spreads

The most reliable thermometer for systemic health is the Credit Spread—specifically, the difference in yield between corporate bonds (often high-yield or "junk" bonds) and risk-free government Treasuries.

When investors are confident, they are willing to lend to riskier companies for a modest premium. However, as the economic outlook darkens or corporate balance sheets face pressure, credit investors demand a significantly higher yield to compensate for the increased probability of default. When this spread begins to widen—often months before the equity markets peak—it is an early warning that credit conditions are tightening. If the cost of borrowing for the most vulnerable companies rises, the equity of those companies is functionally insolvent, and the contagion eventually spreads to blue-chip indices.

2. The Repo Market and Basis Spreads

The Repurchase Agreement (Repo) market is the essential "plumbing" where banks and institutional investors borrow cash overnight, collateralized by high-quality assets like Treasuries. This is the primary engine of market liquidity.

Repo Rates: If the interest rate for overnight borrowing spikes, it suggests that lenders are hoarding cash and are unwilling to trust the collateral offered by borrowers. This creates a "liquidity crunch" where market participants cannot easily roll over their debt.

Basis Spreads: Monitoring the basis spread—the difference between the cash price of a bond and its futures contract—reveals underlying stresses in hedging. When this gap widens, it indicates that the financial system is struggling to facilitate the "arbitrage" necessary to keep markets liquid.

3. The "Financial Conditions Index" (FCI)

Investors should not rely on a single metric. Instead, they should monitor aggregate measures like the Financial Conditions Index. These indices combine multiple inputs—including credit spreads, swap rates, exchange rates, and equity volatility—into a single, unified signal.

Think of the FCI as the "body temperature" of the economy. When financial conditions move from "easy" to "restrictive," the window for equity growth closes. Watching for a sustained move in the FCI toward restrictive territory often serves as the final confirmation that liquidity has reached a breaking point, and that the equity markets are the next domino to fall.

By shifting your gaze from the price of equities to the price of risk within these plumbing-level metrics, you transform your strategy from reacting to volatility to anticipating the structural shifts that cause it.

The "Smart" Edge: Automating Your Tactical Response

Most investors rely on "gut feeling" to decide when to buy a dip or sit on the sidelines. In a market where credit cracks often precede equity crashes, intuition can sometimes actually be your greatest liability. That is why professional traders are increasingly moving toward rule-based tactical strategies that remove human emotion from the equation.

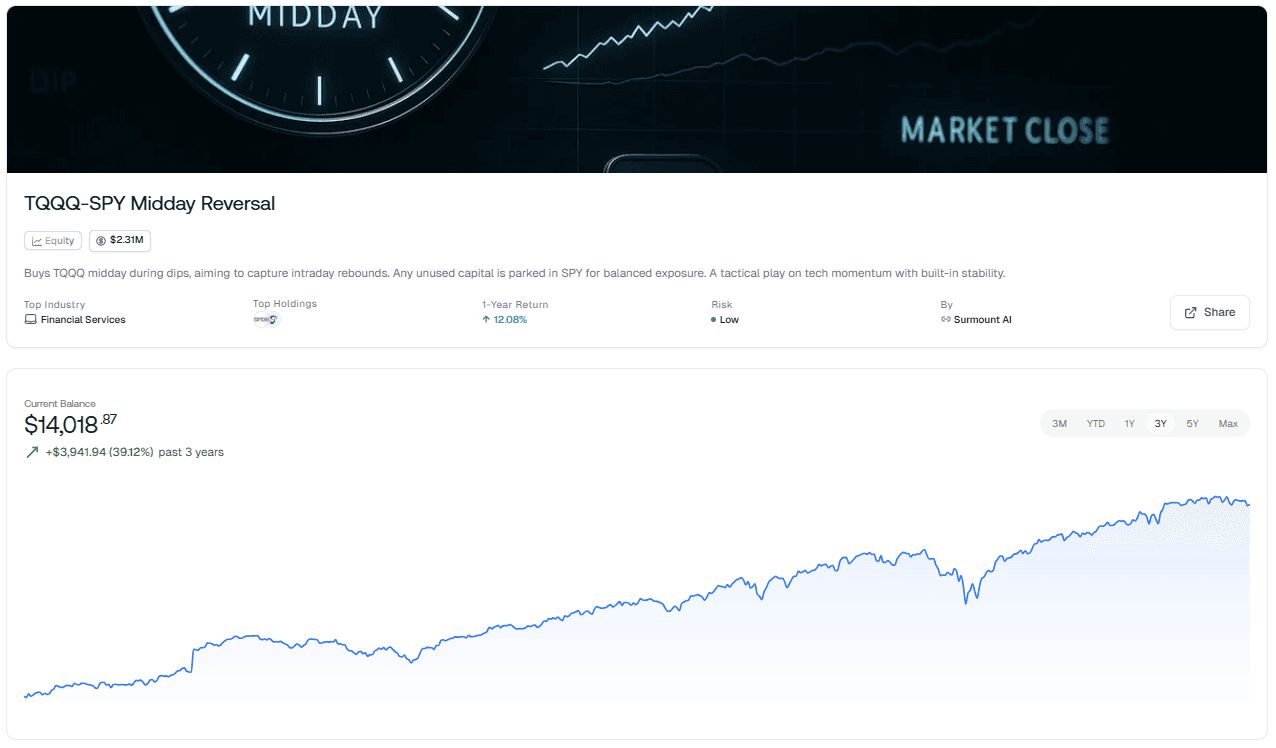

This is where Surmount’s low-risk “TQQQ-SPY Midday Reversal” comes into play.

This strategy is designed for the modern, risk-conscious investor who understands that the market isn't just about picking winners—it's about managing exposure.

Why This Strategy Is Built for Current Markets:

Mechanical Discipline: By targeting TQQQ specifically on intraday dips, the algorithm avoids the trap of "buying into a crash" based on hope. It executes only when technical conditions align, effectively harvesting the rebound volatility that others fear.

Intelligent Cash Management: We don’t just hold SPY blindly. By utilizing a "parked capital" approach, we ensure that your money is always working for you in a liquid, broad-market index, but—most importantly—this is a modular design. You can easily integrate a "Credit Spread Filter" that forces the system to rotate from SPY into cash or short-term Treasuries the moment the credit markets signal systemic stress.

The Best of Both Worlds: You get the upside momentum of tech when the market is healthy, paired with the stability of a broad-index parking spot. It’s not just "trading"—it’s quantitative asset allocation that adapts to the reality of the market's plumbing.

Take Control of Your Portfolio

Stop guessing where the market is going and start building a system that reacts to the signals that matter. Whether you are looking to capture short-term rebounds or optimize your idle capital, our strategy provides the framework you need to stay ahead of the curve.

Automate any portfolio using data-driven strategies made by top creators & professional investors. Turn any investment idea into an automated, testable, and sharable strategy.