Surmount Review 2026: Is It Worth It for Automated Investing?

Surmount Blogs

Surmount review 2026: Is automated investing worth it? We tested it for 30 days. See pricing, features, pros, cons & how it compares to rivals.

Surmount Review 2026: Is It Worth It for Automated Investing?

We spent 30 days using Surmount across multiple brokerage accounts — running pre-built strategies, testing the AI builder, and watching how execution held up in a volatile market. This Surmount review covers what works, what doesn't, and who it actually makes sense for.

The short answer: it's a well-designed platform with a genuine edge over robo-advisors, especially if you want rules-based automation without writing a line of code. But it's not for everyone, and a few rough edges are worth knowing before you sign up.

What is Surmount?

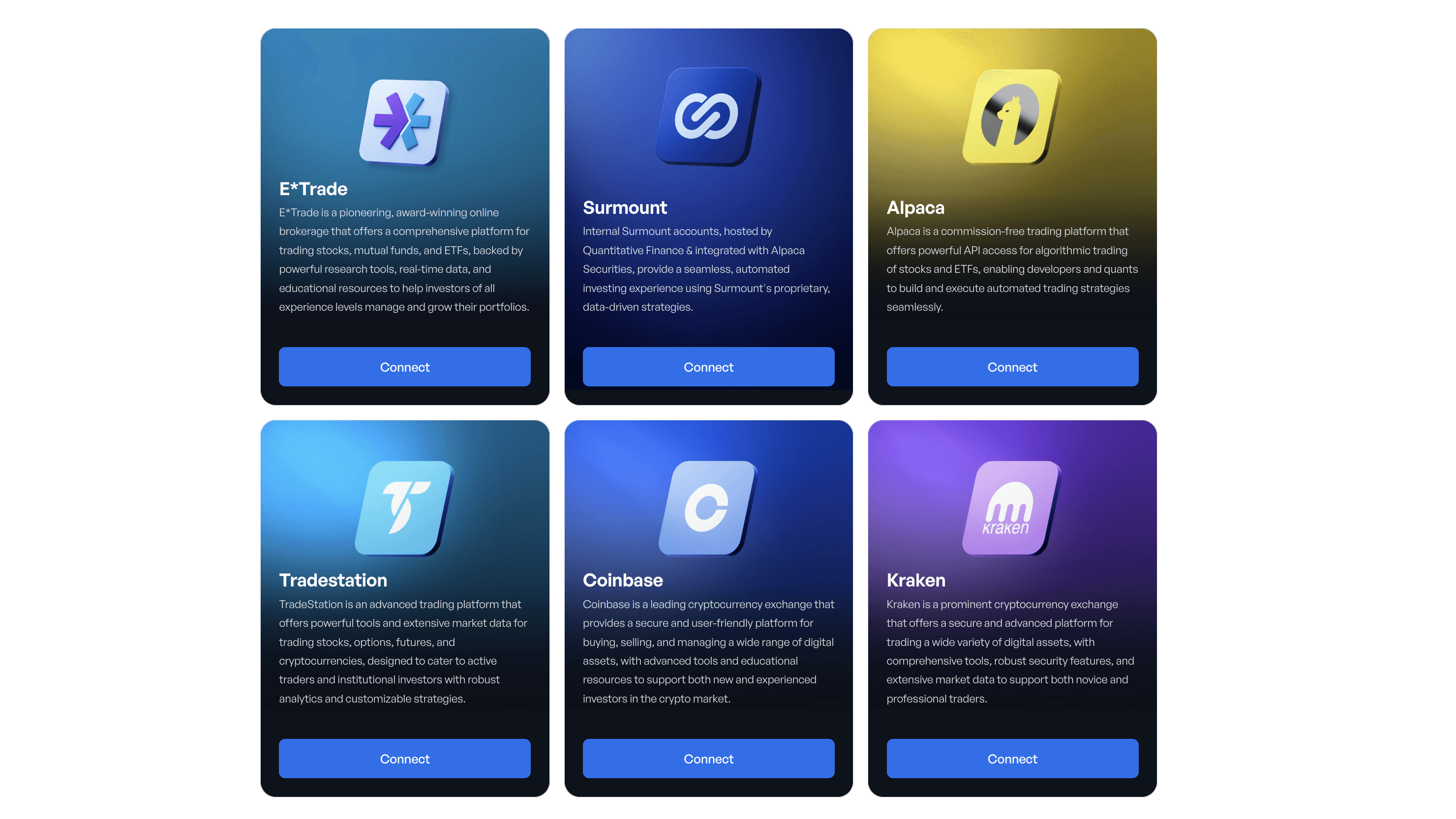

Surmount is an automated investing platform that lets you connect your existing brokerage accounts and run data-driven strategies — either pre-built by quants, custom-built by you, or generated by AI. It's not a broker. It doesn't hold your money. It connects to your account at Alpaca, Robinhood, Interactive Brokers, and others, then executes trades on your behalf based on the strategy you select.

Think of it as a strategy layer that sits on top of wherever you already invest.

Who Is Surmount For?

Surmount works best for three types of users:

Surmount works best for three types of users:

Self-directed investors who want automation without coding. If you have a thesis — "I want a momentum strategy that rotates out of equities when volatility spikes" — Surmount lets you build and run that without touching Python.

Active investors tired of manual rebalancing. If you're managing your own portfolio but find yourself making emotional decisions or missing rebalance windows, the automation layer solves that directly.

Curious beginners who want more than index funds. The strategy marketplace gives you access to back-tested, professionally built strategies from $5/month. That's a meaningful unlock if you've only ever done buy-and-hold.

It's not the right fit if you want a fully hands-off robo-advisor that picks everything for you. Surmount rewards people who have an opinion about how they want to invest.

Key Features of the Surmount Investing Platform

Strategy Marketplace

The marketplace is the core product. You browse strategies built by quants and professional traders, each with a verified track record and backtest data. You connect a strategy to your brokerage account and it runs automatically from there.

What separates this from copy-trading apps is transparency. You see the logic behind each strategy, not just the returns. That matters if you want to understand what you're running in your portfolio.

ETF Builder

Surmount's ETF Builder lets you create a custom, rules-based portfolio of ETFs — similar to building a pie in M1 Finance, but with the ability to add allocation rules, rebalancing triggers, and conditional logic. You're not just picking weights; you're deciding how and when the portfolio adjusts.

Promptfolio

This is the AI-powered strategy builder. You describe your investment thesis in plain language — "I want exposure to AI infrastructure companies with a momentum filter and a cash buffer in downturns" — and Surmount's AI translates it into an executable strategy. It's still a newer feature and works best when your thesis is specific rather than vague.

Broker Connectivity

Surmount connects to a wide range of brokers including Alpaca, ETrade, Coinbase, and others. Strategies are broker-agnostic — you don't need to rebuild your setup if you switch brokers. See the full broker list here.

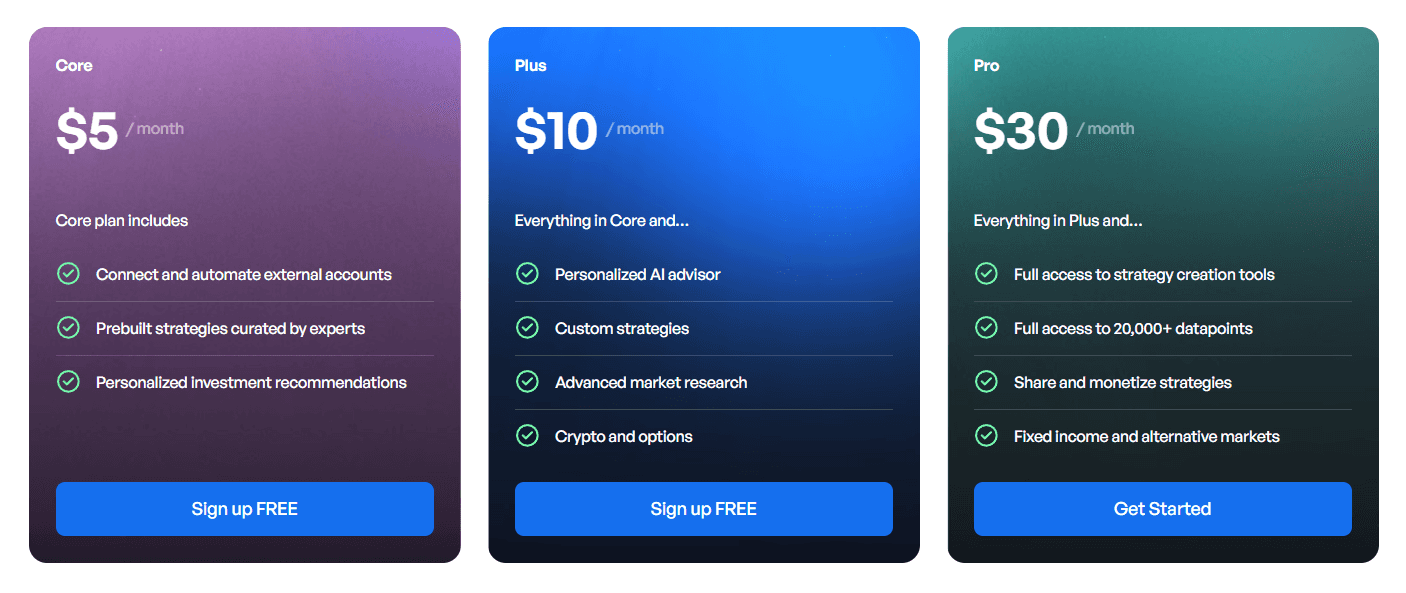

Surmount Pricing Breakdown

There are four tiers, and the entry point is genuinely low for what you get.

Free — $0/month, free forever

Create and fund a Surmount account, invest directly via Surmount (1% management fee applies), access the Dashboard for Surmount accounts, explore the Marketplace, and use the Markets page for research, screeners, and insights.

Core — $50/year (2 months free)

Everything in Free, plus the ability to connect and invest in external accounts (up to $50,000), access the Dashboard for both external and Surmount accounts, free strategy templates, and full Marketplace and Markets page access. Unlimited investment to internal accounts (1% management fee applies).

Plus — $100/year (2 months free)

Everything in Core, plus an increased external account investment limit of up to $150,000, and access to the No-Code Strategy Builders including the ETF Builder and No-Code Strategy Builder. Includes the Create tab for no-code strategy building.

Pro — $300/year (2 months free)

Full feature access. Invest unlimited amounts across internal, external, and paper accounts (1% management fee applies on internal accounts). Use all strategy builders including the No-Code builder, Code builder, ETF builder, and Promptfolio. Access to Dashboard, Marketplace, and Strategies. Use Paper Trading for testing ideas, and full access to the Markets page.

No hidden fees, no percentage-of-AUM charge on subscription tiers. You pay a flat annual subscription and keep all of your returns. See the full breakdown at surmount.ai/pricing.

Surmount Review: The Pros

1. Flat-fee pricing with no AUM cut.

A 0.25% fee on a $100K portfolio costs $250/year. Surmount Pro costs $300/year and doesn't scale with your balance. For larger portfolios, this math gets better fast.

2. You keep your existing broker.

No account transfer required. This removes a major barrier to entry and means you're not locked in.

3. Pre-built strategies with real track records.

The marketplace shows actual performance history, not just hypothetical backtests with cherry-picked parameters. That's a meaningful trust signal.

4. Promptfolio lowers the floor.

The ability to describe a strategy in plain language and have it built automatically opens the platform to people who have a thesis but not the technical skills to execute it.

5. No emotional interference.

The whole point of rules-based automation is removing the impulse to sell during a dip or chase a rally. Surmount executes the strategy; you don't have to act on market noise.

The Cons (Worth Knowing)

1. The strategy library is still growing.

Compared to a more established platform, the number of available strategies in the marketplace is limited. If you have a super niche thesis, you may need to build your own.

2. Promptfolio works best with specific inputs.

Vague prompts produce vague strategies. You'll get better results if you have a clear thesis going in, which means some investment literacy is assumed.

3. U.S.-focused.

Surmount's broker connections and regulatory structure are primarily U.S.-based. International investors have limited access.

3. It's not a robo-advisor.

If you want something to manage everything with zero decisions on your part, this isn't it. Surmount works best for investors who want to be in the driver's seat, just with better tools.

How Surmount Compares

Surmount vs. Composer

Composer is Surmount's closest competitor — both target self-directed investors who want algorithmic strategies without code. The main differences are pricing and flexibility. Composer charges a percentage of AUM above certain thresholds, which gets expensive at scale. Surmount's flat-fee model is more predictable. Surmount also has broader broker connectivity, while Composer routes through its own brokerage. See the full Composer comparison here.

Surmount vs. M1 Finance

M1 Finance is built around "pies" — static, weighted portfolios that rebalance passively. It's a solid set-and-forget product. Surmount's ETF Builder covers similar ground but adds rules-based logic, dynamic rebalancing triggers, and conditional allocation shifts. If you want your portfolio to actually respond to market conditions rather than just drift back to target weights, Surmount has the edge. See the M1 Finance comparison here.

Surmount vs. Betterment

Betterment is a true robo-advisor — it makes all the decisions for you based on a risk questionnaire. That's the right product for investors who don't want to think about strategy at all. Surmount is for investors who want automation on their terms. You're not handing the wheel over; you're adding cruise control. Different product for a different mindset.

Our Verdict on This Surmount Review

For self-directed investors who want to stop managing their portfolio manually without losing control of how they invest, Surmount is one of the best-built tools available at this price point. The flat-fee structure, broker agnosticism, and strategy marketplace are all genuine advantages over alternatives.

The platform is still maturing — the strategy library is growing and some AI features are newer — but the foundation is solid and the team ships updates consistently.

If you have an investment thesis and want to execute it systematically, Surmount is worth trying. The free trial removes the risk.

Frequently Asked Questions

Is Surmount legit?

Yes. Surmount's investment advisory operations run through Quantbase, LLC, a wholly-owned subsidiary registered as an investment adviser with the SEC. Your assets stay at your existing broker — Surmount doesn't hold funds.

Is Surmount safe?

Your investments remain in your own brokerage account. Surmount connects via read/write API using bank-level security, and you can revoke access at any time. The platform doesn't custody assets.

What is a Surmount investing review compared to other robo-advisors?

Unlike robo-advisors, Surmount gives you control over strategy selection and logic. You're not filling out a risk questionnaire and accepting a generic portfolio — you're choosing or building rules-based strategies that match your view of the market.

Can I use Surmount with my existing brokerage?

Yes, in most cases. Surmount connects to Alpaca, Interactive Brokers, Robinhood, and other major brokers. See the full list at surmount.ai/brokers.

How much does Surmount cost?

Plans start at $5/month for Core, $10/month for Plus, and $30/month for Pro. No AUM fees. Full details here.

What happens if I want to cancel?

Surmount has no lock-in. You can cancel your subscription at any time with no penalties.

We hope this Surmount AI review was insightful. If you are interested, start your free trial now!

Automate any portfolio using data-driven strategies made by top creators & professional investors. Turn any investment idea into an automated, testable, and sharable strategy.