Shorting Private Credit: When It Works and When It Backfires

Surmount Blogs

An overview of the risks and mechanics of shorting private credit, explaining crowded proxy trades, valuation lags, refinancing cliffs, and lender-driven restructuring tactics.

Shorting Private Credit: When It Works and When It Backfires

The period between mid-2023 and early 2025 have been called the golden age of private credit markets. This designation was largely driven by a "perfect storm" of macroeconomic factors that created uniquely favorable conditions for non-bank lenders which saw sustained yield expansion:

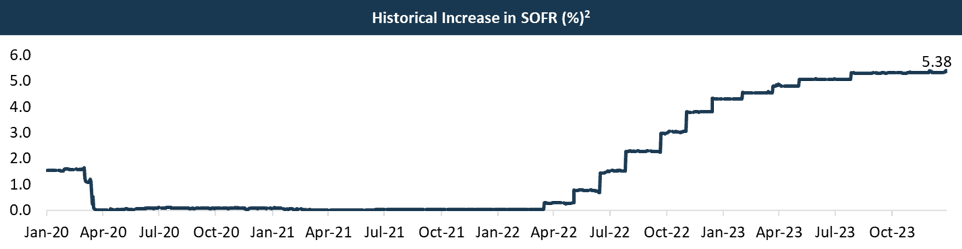

With the Federal Funds Rate holding at a plateau, Private Credit (PC) funds captured double-digit coupons on senior secured paper—returns historically reserved for the bottom of the capital stack.

However, this golden age turned out to be short lived, as hidden cracks within the market began to spider. These included spikes in PIK interest rates, and severe spread compression as traditional banks aggressively re-entered the market.

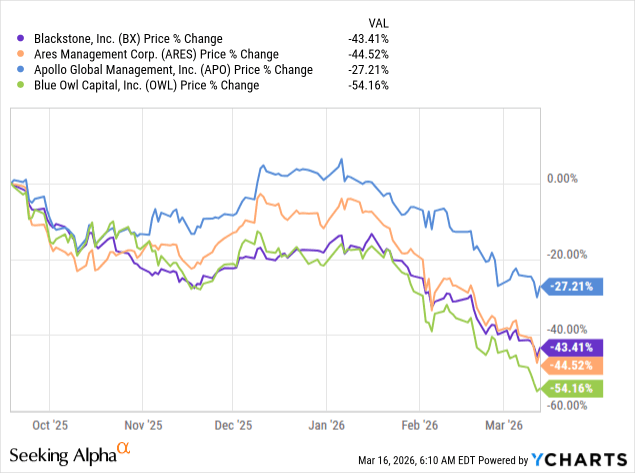

Fast forward to March 2026, the market faces a meltdown that few had anticipated. This is evident in the selloffs impacting some of the most prominent private equity stocks:

For the tactical investor, this environment presents the ultimate "anti-consensus" opportunity. However, shorting this space is not as simple as betting against a ticker. It requires an understanding of the Lender-on-Lender violence now occurring in the shadows, where "Agreement-to-Agree" clauses are being weaponized and senior-secured status is being stripped through aggressive "uptiering" maneuvers.

To understand why this trade is currently one of the most crowded—and dangerous—on the Street, we must first look at the mechanics of the "Liquidity Trap" that has been set over the last eighteen months.

The Mechanics of the "Crowded" Short

The primary challenge in shorting private credit is that it is essentially a "dark" asset class. Because these loans do not trade on public exchanges, you cannot simply borrow the paper and sell it short. This structural opacity forces participants to build "synthetic" short positions, which creates high-conviction, high-crowding environments.

In particular, investors are dealing with three structural issues here:

The Proxy Problem

Because direct shorts are impossible, the market converges on a handful of liquid proxies. When sentiment sours, everyone rushes to the same exit:

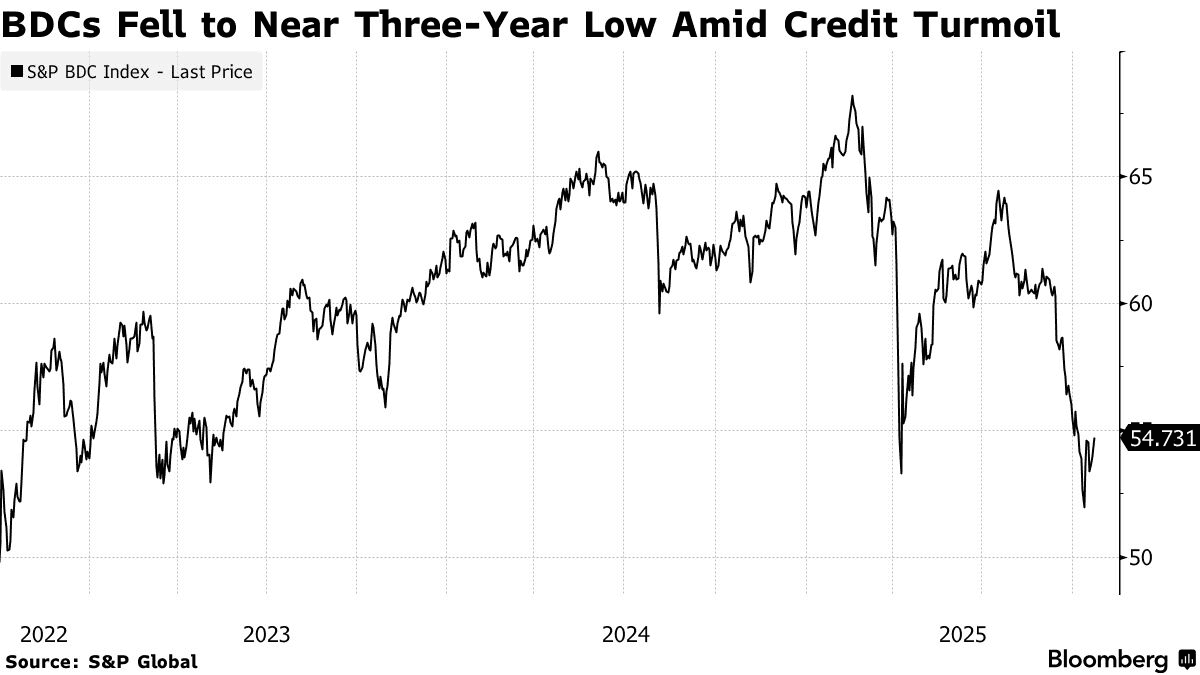

Shorting BDCs (Business Development Companies): This is the most common, yet dangerous, play. BDC stocks often trade as a proxy for the entire private credit market. When investors want to short "private credit," they sell BDC shares. This causes price dislocations, as were seen in 2025, that had nothing to do with the credit quality of the underlying loans and everything to do with liquidity-driven selling.

CDS on Leveraged Loans: Sophisticated players attempt to use Credit Default Swaps (CDS) on broadly syndicated loan indices (like the LCDX). However, because the underlying private credit loans are often covenant-lite or bespoke, the correlation between the liquid index and the private portfolio is often weak—meaning the short can be wrong even when the credit market is melting down.

The Valuation Lag (The "Ghost" Risk)

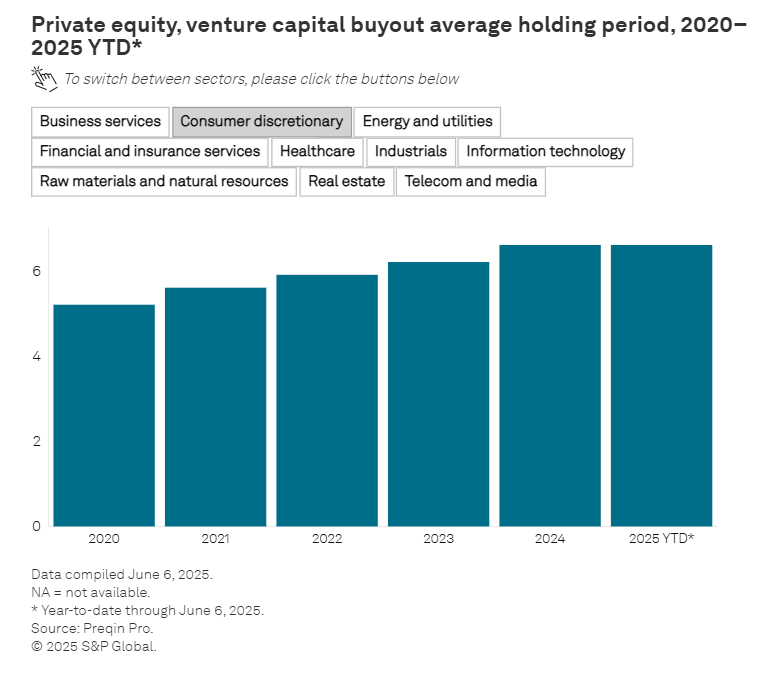

A critical reason this trade becomes crowded is the Quarterly Valuation Gap. In recent years, owing to inflated valuations, holding durations are extending:

Because private assets are marked to model rather than marked to market, they exhibit "low volatility" by design. A short-seller may be intellectually correct that a portfolio is impaired, but if the manager hasn't yet written down the assets, the short-seller must endure months of paying "carry" (or funding the short) while the public market moves against them.

This creates a trap: the trade only becomes "profitable" once the accounting catch-up happens, by which time the trade is usually fully priced in and overcrowded.

The Refinancing Cliff Synchronization

Crowding is intensified by the "calendar effect." Most private credit portfolios have lumpy maturity profiles. When a wall of debt matures simultaneously, the entire asset class enters a "refinancing squeeze." As lenders pull back or demand stricter terms, all sponsors realize at once that their capital structures are unsustainable.

The sudden scramble for liquidity causes a synchronized drop in sentiment, leading to a massive, crowded rush to hedge or exit positions that were previously ignored.

When Shorting Private Credit Backfires: The "Gamer" Dynamics

Shorting private credit is rarely about being "right" on the fundamentals of the underlying business; it is about being able to survive the structural warfare deployed against you. When the trade backfires, it is usually because the short-seller underestimated the non-market mechanisms that keep a deal from hitting the floor.

The Sponsor’s Toolkit: "Equity Cures" and Zombie Management

In public markets, a default is a default. In private credit, a default is much more complicated. Private Equity (PE) sponsors have a vested interest in preventing a credit event that would trigger a default clause, as it would force a mark-down of their own funds.

Typically, sponsors often have the flexibility to inject capital into a distressed asset at the eleventh hour to keep it current. For a short-seller, this is a nightmare—the "default" you were betting on disappears overnight, and the cost of maintaining the short position remains unchanged.

Similarly, because lenders and sponsors often sit on the same side of the table (and sometimes share common investors), there is a massive incentive to modify covenants rather than accelerate a loan. So short-sellers would effectively be betting against the entire ecosystem's desire to avoid a public loss, and not just against a company.

The Cost of Being Early: The "Carry" Trap

One more thing to keep in mind is that the math of the short is inherently punishing. Private credit yields are high, and the "proxy" instruments you are using (like BDCs or credit ETFs) often pay out attractive dividends.

While you wait for the "valuation catch-up" or the wave of defaults, your P&L is being bled by the carry. This is called negative carry.

On the other hand, there is the risk of a classic squeeze. If a broad market recovery occurs while you are waiting, the very instruments you are short will likely rally, forcing you to cover at a loss before the fundamental thesis—the eventual credit deterioration—ever has a chance to play out.

Lender-on-Lender Violence: The "Uptier" Threat

The most sophisticated danger to a short-seller is the evolution of "liability management exercises" (LMEs). One form of this is structural subordination. This refers to large credit funds forming ad-hoc groups to "uptier" their existing debt. They essentially move their debt to a new entity with better collateral or priority, stripping the existing lenders (or the proxy instruments you might be shorting) of their seniority.

Similarly, there is the “Out of Court” risk. This maneuvering happens in private, away from the scrutiny of the SEC or public market watchdogs. By the time the news hits the wire, the value of the paper you are shorting has been gutted by a maneuver you didn't even know was legally possible.

Ultimately, shorting private credit backfires because it assumes the market is a price discovery mechanism. In reality, private credit is a negotiation mechanism. If you are looking to short this space, you must differentiate between "distressed balance sheets" and "distressed entities that have no path to a negotiated solution."

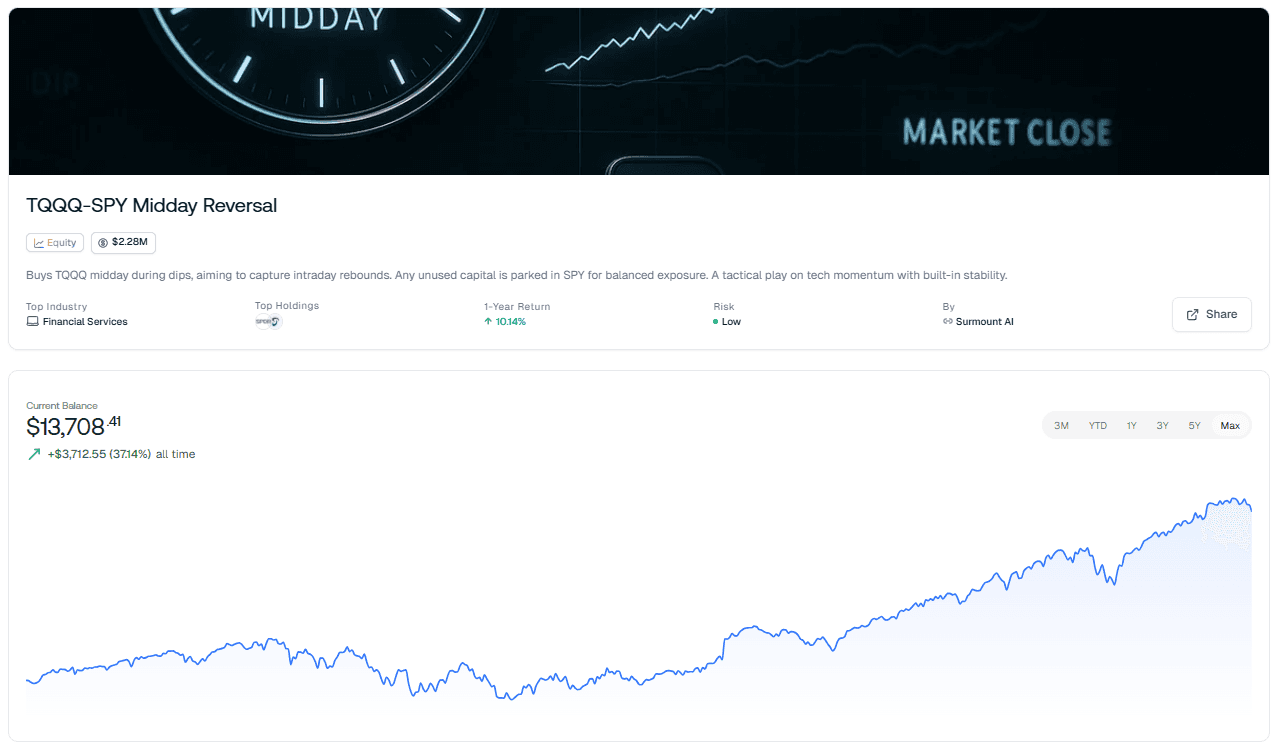

Tactical Momentum via the TQQQ-SPY Midday Reversal

If shorting private credit is a "widowmaker" trade due to its liquidity traps, valuation lags, and sponsor-led "zombie" support, the intelligent investor must ask: Where can I actually capture alpha without fighting the system?

The TQQQ-SPY Midday Reversal strategy offers a superior alternative by focusing on liquid, high-beta assets where price discovery is instant.

Why this is the smarter play:

Liquidity vs. Lockups: Unlike private credit, which is often trapped in opaque, illiquid vehicles, TQQQ and SPY are among the most liquid instruments on the planet. You are never waiting for a quarterly valuation to see your P&L; you are in and out of the market within hours.

Asymmetric Volatility: Instead of waiting for a credit collapse that may never come (due to sponsor intervention), this strategy thrives on volatility. By entering TQQQ during midday dips, you are capturing the "washout" phase of the day—the exact moment when weak hands capitulate.

Balanced Exposure: By parking unused capital in SPY, you maintain core market exposure. This provides a "shock absorber" for your portfolio, allowing you to stay invested in the broader market while using a small, tactical sleeve to harvest intraday tech momentum.

Deploy Your Edge

Stop waiting for a "black swan" in the private credit market that may never trigger the way you expect. Start capturing the volatility you already see every day.

Automate any portfolio using data-driven strategies made by top creators & professional investors. Turn any investment idea into an automated, testable, and sharable strategy.