What Makes an Alternative Investment Work in Your Portfolio

Surmount Blogs

Institutional investors use alternatives for portfolio function—not hype. Learn how retail investors can apply this framework with crypto, private equity, and direct indexing.

When institutional investors allocate to alternative investments—whether private equity, real estate, or even cryptocurrency—they don't simply ask "should I buy this?" Instead, they ask a more sophisticated question: "what role does this serve in my portfolio?"

It's a subtle distinction that makes all the difference. And it's exactly what separates thoughtful portfolio construction from speculative gambling.

The Widening Gap Between Institutional and Retail Alternative Allocations

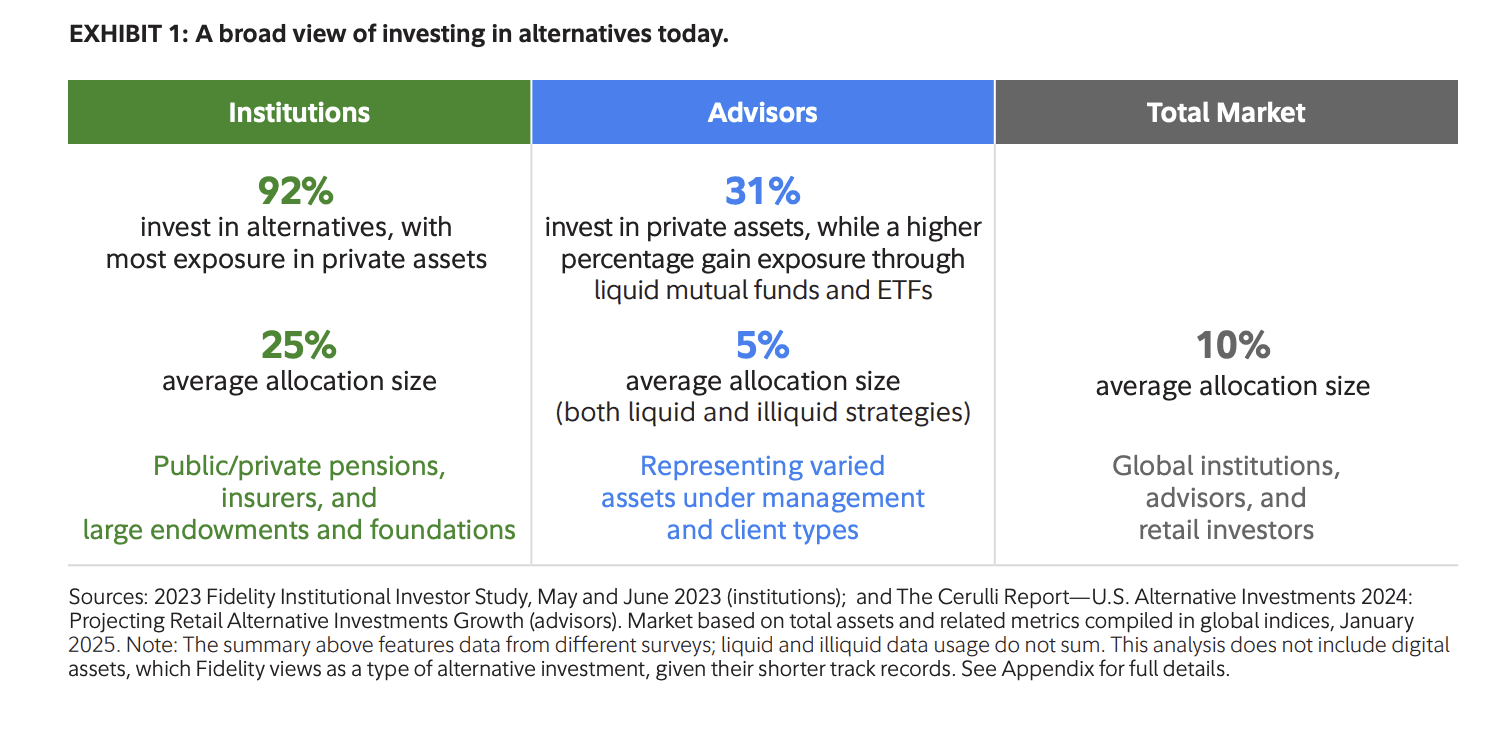

The numbers tell a stark story. Institutions currently allocate an average of 25% to alternative investments, while retail investors—guided by financial advisors—average just 5%. This five-fold difference isn't merely about access or minimums anymore. It's increasingly about philosophy.

For decades, alternative investments were the exclusive domain of endowments, pension funds, and ultra-high-net-worth families. High minimums—often $1 million or more—created natural barriers. But that landscape has fundamentally shifted. Retail investors now have access to alternatives through interval funds, business development companies, and semi-liquid structures, with assets in these vehicles reaching $1.1 trillion as of March 2024.

Yet access hasn't translated to adoption. Despite growing availability, only 31% of financial advisors report allocating to illiquid alternatives on behalf of their clients. The democratization of alternatives is happening, but the democratization of alternatives thinking has lagged behind.

What Institutional Investors Understand About Portfolio Function

Walk into any endowment meeting or pension committee discussion, and you'll notice something: they don't talk about assets in isolation. They talk about portfolio roles.

Institutional investors allocate 27% to alternatives on average across pensions and large endowments, but these allocations serve distinct purposes:

Private equity (averaging 6-9% of institutional portfolios): Return enhancement and illiquidity premium capture

Private credit (2-4% allocations): Income generation with structural protections

Real estate and infrastructure (9-11% combined): Inflation hedging and cash flow stability

Hedge fund strategies (3-5%): Risk management and non-correlated returns

Each allocation decision emerges from a clear understanding of what the institution needs, not what's performing well at the moment. The largest endowments and foundations hold 9% in private equity and 5% in hedge fund strategies because their infinite time horizons and low spending requirements allow them to harvest illiquidity premiums that shorter-horizon investors cannot.

Contrast this with retail portfolios, where alternatives—when they appear at all—often enter opportunistically rather than systematically. An advisor hears about a private credit fund with attractive yields. A client reads about private equity returns. Bitcoin surges and suddenly crypto becomes "a good investment."

Missing from these decisions: what functional role does this serve?

The Crypto Case Study: Access Without Understanding

Nothing illustrates this gap more clearly than cryptocurrency allocation decisions.

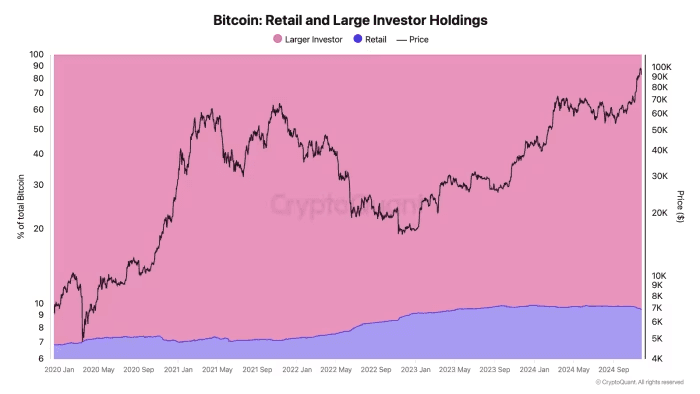

Bitcoin ownership remains 85% retail and just 15% institutional, according to Bitwise—the inverse of S&P 500 ownership patterns. Yet the way these two investor cohorts approach crypto couldn't be more different.

When institutional investors consider cryptocurrency allocations, research from VanEck demonstrates they focus on risk-adjusted optimization within specific volatility bands. Their analysis shows that a 3% Bitcoin and 3% Ethereum allocation in a traditional 60/40 portfolio produced the highest Sharpe ratio while maintaining acceptable volatility levels—a maximum 6% combined exposure.

BlackRock's sizing framework similarly recommends 1-2% Bitcoin allocations, noting that this range contributes roughly the same portfolio risk as a single "Magnificent Seven" tech stock position. The logic is deliberate: institutions size crypto not by upside potential but by acceptable portfolio risk contribution.

Retail approaches, by contrast, often swing between extremes—either avoiding crypto entirely or making concentrated bets that dominate portfolio risk. Surveys show retail crypto allocations averaging 25.7% of investment portfolios when allocated at all, far exceeding the measured institutional approach.

The difference isn't risk tolerance. It's framework. Institutions ask: "Given our existing exposures and constraints, what incremental risk-adjusted benefit does a small crypto allocation provide?" Retail investors too often ask: "Is crypto going up?"

Why Portfolio Function Matters More Than Performance

The irony of chasing performance in alternatives is that it often leads to exactly the wrong timing. Consider private equity, which institutional analysis shows has outperformed public markets by nine percentage points annually over five-year periods. Yet these same institutions don't view private equity purely as a return maximizer.

Large endowments allocate 9% to private equity despite acknowledging that implementation complexity, manager selection risk, and capital commitment requirements create operational burdens. They accept these frictions because private equity serves a specific role: capturing the illiquidity premium and accessing growth in private companies that now represent 87% of U.S. companies with $100+ million in revenue.

Similarly, real estate allocations averaging 6-7% across institutional portfolios exist not because institutions expect explosive returns, but because real assets provide inflation correlation and cash flow characteristics that public equities cannot replicate. Returns for closed-end real estate funds registered -1.1% through Q3 2024, yet institutions maintained allocations because the function remained valuable even when returns disappointed.

This functional thinking explains why institutional investors showed under-allocation to private credit despite forward-looking return expectations of 6.6%. Years of low rates had shifted allocations toward private equity's equity-like returns. As rates normalized, institutions recognized private credit's portfolio role had changed—but allocation adjustments followed function analysis, not headline performance.

The Direct Indexing Revolution: Building With Any Building Block

The gap between institutional and retail alternative investing isn't just philosophical—it's increasingly technological. And direct indexing platforms represent a bridge.

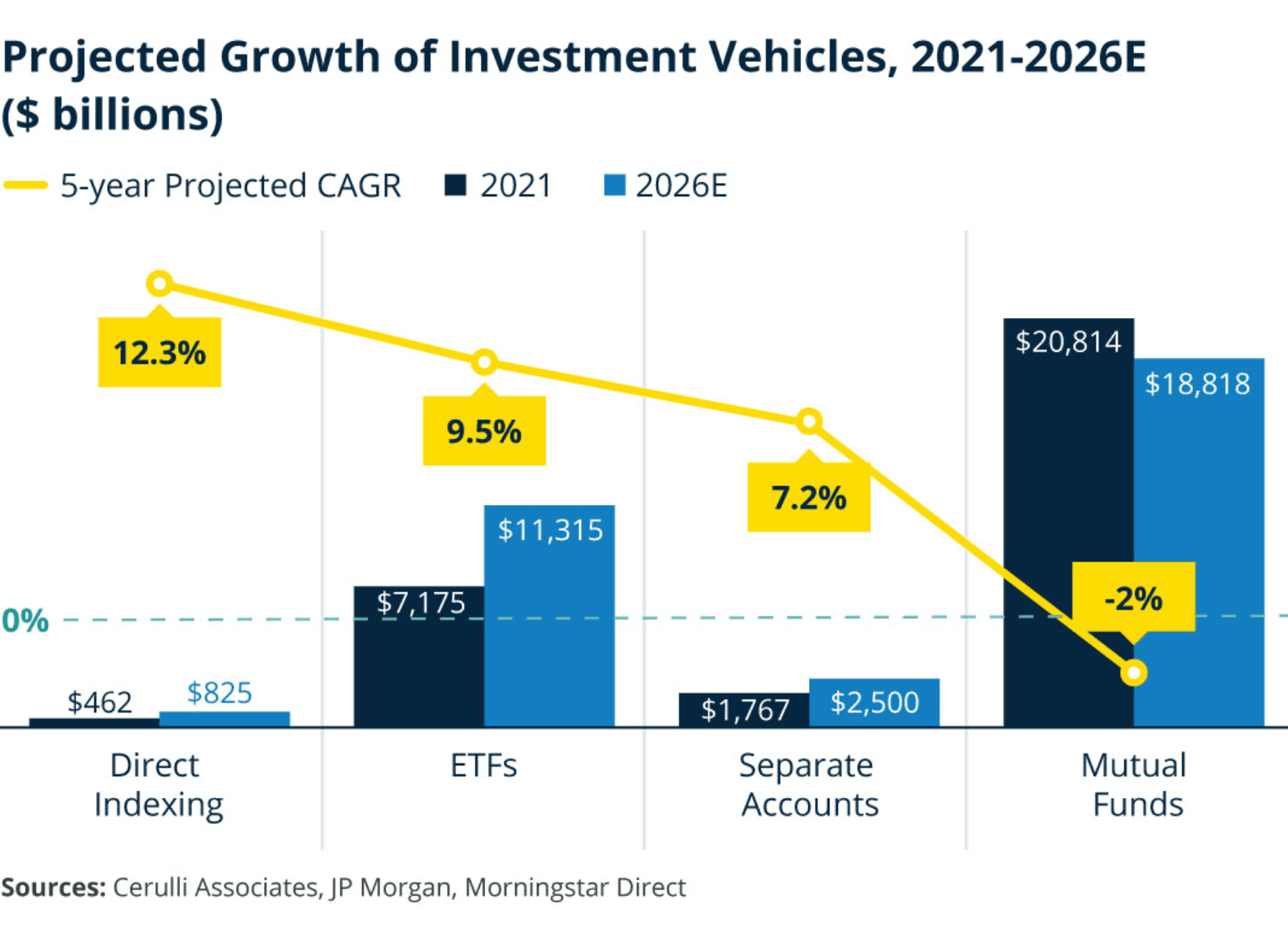

Direct indexing assets reached $864.3 billion by year-end 2024, growing at a 22.4% compound annual rate since 2021. Yet only 18% of financial advisors currently use these strategies, and another 12% don't even know what direct indexing is.

What's revolutionary about direct indexing isn't just tax-loss harvesting—though research suggests this could boost returns by 2.15-2.66 percent annually. It's the ability to construct portfolios with institutional-grade intentionality, regardless of asset class.

Modern platforms allow investors to:

Build custom indices across any asset class: Not just equities, but sector-specific exposures, thematic baskets, or even alternative beta strategies

Apply consistent risk frameworks: Size allocations based on portfolio risk contribution rather than arbitrary percentages

Implement values-based constraints: Exclude specific securities while maintaining diversified market exposure

Harvest tax benefits systematically: Manage gains and losses at the individual security level

This transforms portfolio construction from product selection to strategy assembly. Instead of choosing between Fund A and Fund B, investors can build the exposure they need with the characteristics they want.

For alternatives, this shift is profound. Rather than accessing private equity through a single high-fee fund, investors might construct private company exposure through multiple vehicles—a direct lending interval fund, a BDC for mid-market credit, a semi-liquid private equity structure—each sized to serve a specific portfolio function.

Surmount: Institutional Portfolio Construction, Democratized

This is where platforms like Surmount become essential. By offering both pre-built expert strategies and custom portfolio construction tools, Surmount enables the institutional question—"what role does this serve?"—at the retail level.

The platform's power lies in its flexibility:

For investors seeking guidance: Access professionally constructed strategies that incorporate alternatives with clear portfolio roles—whether that's a 5% allocation to private credit for income enhancement or a 2% crypto position for non-correlated returns

For sophisticated investors: Build custom direct indices that blend traditional and alternative exposures according to personal risk frameworks, tax situations, and conviction levels

For any asset class: Whether public equities, sector ETFs, alternative mutual funds, or semi-liquid structures, construct portfolios that reflect true diversification—not just across assets, but across return drivers and risk factors

The distinction between retail and institutional investing has never been about intelligence or sophistication. It's been about access to tools and frameworks that allow for thoughtful, role-based portfolio construction.

The Critical Questions to Ask

Before allocating to any alternative investment—whether crypto, private equity, real estate, or hedge strategies—consider:

What portfolio gap does this fill?

Are you seeking return enhancement, downside protection, inflation hedging, income generation, or pure diversification? If you can't articulate the role, you're not investing—you're speculating.

How does this interact with existing holdings?

Institutional investors use correlation analysis and risk attribution to understand how alternatives complement public market exposures. Your concentrated tech stock position might make infrastructure allocations more valuable than additional equity exposure.

What's my implementation edge?

Manager selection drives significant dispersion in alternative returns. Without access to top-quartile managers or a strategy for identifying them, you may not capture the returns that make alternatives compelling.

What's the right size given my constraints?

Time horizon, liquidity needs, tax situation, and emotional tolerance all matter. An allocation that consumes 15% of your portfolio but represents 40% of your risk might be precisely wrong, regardless of expected returns.

How will I rebalance and adjust?

Alternatives lack daily pricing and trading liquidity. Have you considered how you'll manage exposure changes, capital calls, or tactical tilts within illiquid positions?

Building Smarter Portfolios in 2025

The next decade of investing won't belong to those who chase the highest-returning alternative asset. It will belong to investors who think institutionally about portfolio construction—asking functional questions, managing total portfolio risk, and leveraging technology to implement sophisticated strategies.

Alternative assets are projected to reach $30 trillion by 2035, with retail investors driving organic growth. This democratization creates opportunity, but only for those who approach alternatives with the rigor institutions have always applied.

The tools exist. Direct indexing platforms, custom portfolio construction technology, and accessible alternative structures have eliminated historical barriers. What remains is the more fundamental challenge: shifting from opportunistic allocation to functional portfolio design.

Whether crypto, private equity, real estate, or any other alternative, the question isn't "should I invest in this?" The question is "what role does this serve in my portfolio—and is this the optimal way to fill that role?"

Answer that question thoughtfully, and you're no longer investing like retail. You're investing like an institution.

Automate any portfolio using data-driven strategies made by top creators & professional investors. Turn any investment idea into an automated, testable, and sharable strategy.