Walk-Forward Analysis vs. Backtesting: Pros, Cons, and Best Practices

Surmount Blogs

Walk-forward analysis vs. backtesting: Learn which validation method suits your trading strategy, avoid overfitting traps, and implement best practices for robust system development.

Every quantitative trader has experienced that sinking feeling: a strategy performs beautifully in historical testing, only to crumble when real capital enters the picture. This disconnect between past performance and future results represents one of the most persistent challenges in algorithmic trading, and it's precisely why the debate between traditional backtesting and walk-forward analysis matters more than ever.

As markets become increasingly sophisticated and competition intensifies, the methods we use to validate trading strategies have evolved from simple historical replays to more nuanced approaches that better simulate real-world conditions. Understanding the strengths and limitations of each methodology isn't just an academic exercise—it's the difference between deploying a robust strategy and falling victim to what traders call "curve fitting."

Why Traditional Backtesting Remains Both Essential and Problematic

Traditional backtesting operates on an appealingly straightforward premise: apply your trading rules to historical data and see what happens. Traders use this approach to evaluate strategies without risking capital, identifying potential strengths and weaknesses before committing funds.

The appeal of traditional backtesting:

Speed and simplicity - Test years of market behavior within hours

Risk-free environment - Evaluate strategies without capital exposure

Rapid iteration - Quickly test multiple hypotheses and variations

Clear metrics - Analyze win rate, profit factor, and maximum drawdown systematically

This accessibility makes traditional backtesting an indispensable tool in every systematic trader's toolkit. You can examine how a strategy might have navigated bull markets, bear markets, and everything in between—all before risking a single dollar.

Yet this same simplicity harbors a dangerous flaw: traditional backtesting creates a single, static view of strategy performance across the entire historical dataset. When traders optimize parameters to maximize returns on this full dataset, they're essentially peeking at the answers before taking the test. The strategy becomes exquisitely adapted to past market noise rather than capturing genuine, repeatable patterns.

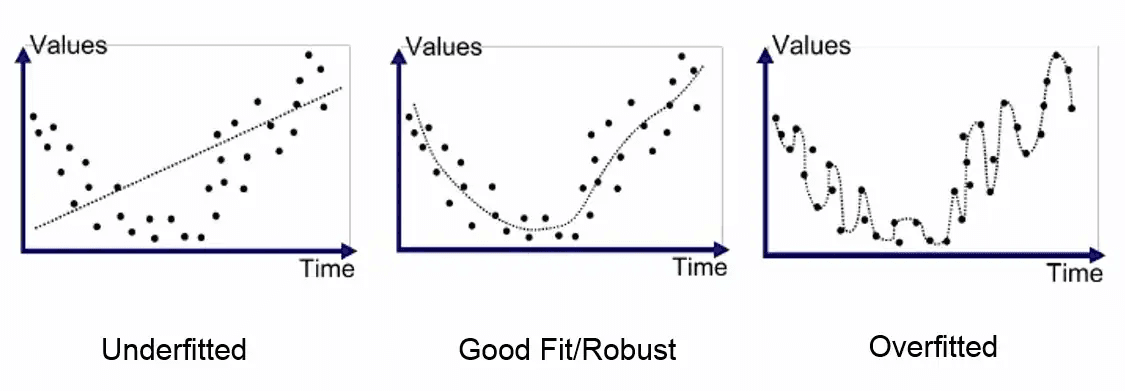

The Overfitting Trap That Derails Most Trading Systems

Overfitting represents the silent killer of trading strategies. It occurs when strategies model random market noise rather than fundamental market behavior, leading to impressive historical results that dissolve under live trading conditions. Think of it as creating a mathematical equation so precisely tailored to past data points that it loses all predictive power for the future.

Why overfitting is so dangerous:

Invisible during development - Curve-fitted strategies can produce stellar Sharpe ratios and minimal drawdowns on paper

Parameter proliferation - More parameters make it easier to inadvertently fit historical quirks that won't repeat

Random patterns appear real - Research has demonstrated even randomly generated strategies can look profitable when excessively optimized

Failure reveals itself late - Problems only become apparent when real money encounters different market conditions

What makes overfitting particularly insidious is that it doesn't announce itself. A curve-fitted strategy can show remarkably consistent returns across historical data, creating false confidence in approaches that hold no genuine edge. The reckoning only arrives when market conditions inevitably differ from the precise historical circumstances the strategy was optimized to exploit.

Academic research into backtest overfitting has revealed that the problem extends beyond obvious parameter manipulation. Even well-intentioned traders engage in what's called "implicit fitting"—making subjective decisions about strategy structure, indicator selection, and rule implementation based on their knowledge of historical outcomes, thereby contaminating the test without realizing it.

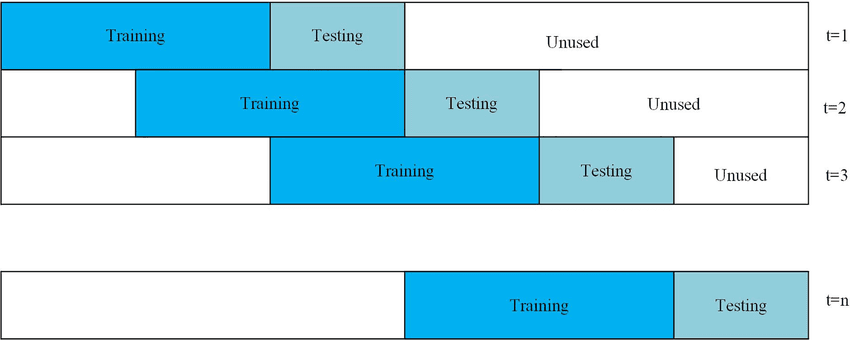

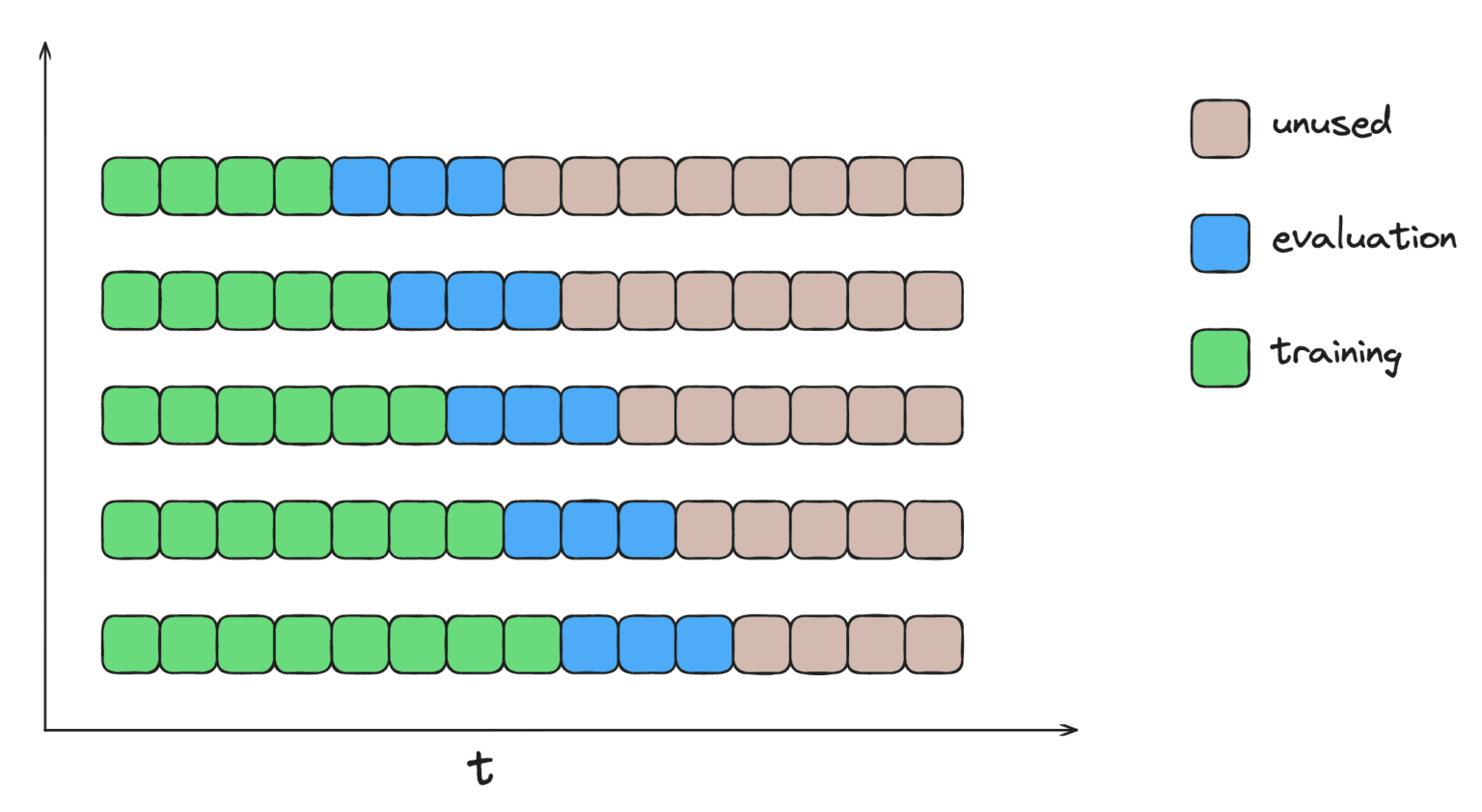

How Walk-Forward Analysis Changes the Validation Game

Walk-forward analysis emerged as a response to traditional backtesting's fundamental weakness. First presented by Robert E. Pardo in 1992, this methodology simulates the actual process of trading a strategy over time by repeatedly optimizing on one period and testing on the next, creating what theorists call a more realistic assessment of strategy robustness.

The walk-forward process in action:

Optimize parameters on historical "in-sample" data (typically several months or years)

Apply those parameters to a subsequent "out-of-sample" period not used in optimization

Roll the window forward and repeat the process across multiple segments

Stitch together results from all out-of-sample periods to create a composite equity curve

This rolling approach addresses backtesting's core limitation: it prevents traders from optimizing on data they'll later use for validation. Each out-of-sample period represents genuinely unseen data at the moment parameters were selected, mimicking the actual challenge traders face when deploying strategies in real markets where future information is unavailable.

The cumulative out-of-sample results create an equity curve that more accurately reflects how a strategy might perform going forward. By providing multiple validation periods across different market conditions, walk-forward analysis reveals whether a strategy's edge persists through varying environments or merely captured fleeting patterns in a single market regime.

The Computational and Conceptual Costs of Walk-Forward Testing

Walk-forward analysis doesn't come free. The repeated optimization cycles create significant computational demands, particularly for complex strategies with numerous parameters. What might take minutes in traditional backtesting can consume hours or days when performing walk-forward analysis, especially when testing multiple parameter combinations across numerous time windows.

The practical challenges:

Multiplied processing time - Each walk-forward window requires its own optimization pass (a 10-year test with monthly windows = 120 separate optimizations)

Hardware requirements - High-frequency strategies or extensive parameter spaces become computationally prohibitive

Window size decisions - The choice of optimization and validation periods introduces new degrees of freedom that can themselves be optimized

Strategy dependency - Walk-forward assumes strategies have parameters worth optimizing

Critics have noted additional subtleties that complicate walk-forward analysis. A strategy might perform well with three-month optimization windows and one-month validation periods but poorly with different window configurations, raising questions about whether impressive walk-forward results reflect genuine robustness or merely fortuitous window selection.

The inherent limitations of parameter-dependent strategies further complicate matters. Walk-forward analysis assumes strategies have parameters worth optimizing. For trading approaches based on market structure or pattern recognition rather than optimizable numerical inputs, the entire walk-forward framework may prove irrelevant or impossible to implement effectively.

Understanding Walk-Forward Efficiency as a Robustness Metric

Walk-forward efficiency (WFE) provides a quantitative measure of how well a strategy's optimization translates to out-of-sample performance. Calculated as the ratio of annualized out-of-sample returns to in-sample returns, this metric offers insight into whether optimization actually improves real-world performance or simply curve-fits historical data.

Interpreting WFE values:

WFE above 50-60% - Strategy maintains at least half its optimized performance on unseen data (suggests genuine robustness)

WFE approaching 100% - Out-of-sample performance matches optimized results (encouraging but warrants investigation)

WFE consistently low - Likely indicates overfitting to historical data

WFE wildly varying - May signal fragility despite acceptable average performance

However, WFE shouldn't be interpreted in isolation. A robust walk-forward analysis examines multiple metrics across validation windows: maximum drawdown consistency, profit factor stability, trade distribution, and win-rate variability. A strategy with high WFE but wildly fluctuating drawdowns across periods may indicate fragility despite good average performance.

The interpretation of WFE becomes more nuanced when considering that markets evolve. Lower WFE doesn't automatically mean a flawed strategy—it might indicate that market conditions genuinely changed between optimization and validation periods, requiring parameter updates to maintain effectiveness. This distinction between overfitting and legitimate market evolution requires careful analysis.

When Walk-Forward Analysis Might Lead You Astray

Despite its theoretical advantages, walk-forward analysis introduces its own failure modes. Perhaps most significantly, traders can engage in what might be called "meta-overfitting"—optimizing the walk-forward process itself by adjusting window sizes, fitness functions, and parameter ranges until the walk-forward results look attractive, thereby defeating the entire purpose of out-of-sample validation.

Common walk-forward pitfalls:

Fitness function shopping - Testing multiple optimization metrics (profit, risk-adjusted return, drawdown) until one produces favorable results

Window size optimization - Adjusting time periods to improve outcomes rather than using predetermined, rational windows

Parameter range fitting - Limiting optimization ranges based on knowledge of what worked historically

Selection bias - Only reporting the strategy with the best walk-forward results after testing dozens of concepts

The choice of fitness function—the metric used to select optimal parameters during each in-sample period—can dramatically influence results. A strategy optimized for maximum profit might produce very different walk-forward outcomes than one optimized for risk-adjusted returns, profit factor, or maximum drawdown minimization. This flexibility creates another dimension where traders might inadvertently overfit by testing multiple fitness functions until finding one that produces favorable walk-forward results.

Window size selection presents similar challenges. Short optimization windows might fail to capture sufficient market conditions, while long windows reduce the number of out-of-sample periods available for validation. Research indicates that walk-forward analysis can exhibit notable shortcomings in false discovery prevention, with increased temporal variability compared to more sophisticated validation methods like Combinatorial Purged Cross-Validation.

The temporal nature of walk-forward analysis also means it cannot protect against certain forms of data mining. If a trader tests dozens of different strategy concepts and only reports the one with the best walk-forward results, the selection bias remains even if each individual strategy underwent proper walk-forward validation. The out-of-sample periods only remain truly out-of-sample for the first strategy tested.

Combining Methodologies for More Robust Strategy Validation

The most sophisticated approach to strategy validation doesn't choose between traditional backtesting and walk-forward analysis—it leverages both within a comprehensive testing framework. This integrated methodology begins with traditional backtesting for rapid strategy development and parameter exploration, then applies walk-forward analysis to validate robustness, before finally employing paper trading to assess real-world execution characteristics.

A layered validation approach:

Stage 1: Traditional backtesting - Quickly eliminate flawed concepts and explore broad parameter ranges

Stage 2: Walk-forward analysis - Validate that promising strategies maintain edge across multiple market regimes

Stage 3: Hold-out sample testing - Reserve final 10-20% of data completely untouched until after all development

Stage 4: Paper trading - Test execution characteristics in live market conditions without capital risk

The sequence matters. Traditional backtesting excels at quickly eliminating obviously flawed concepts, testing theoretical frameworks, and exploring broad parameter ranges. Once a strategy shows promise in initial backtests, walk-forward analysis provides deeper validation across multiple market regimes, revealing whether the edge persists when parameters are selected without foreknowledge of subsequent performance.

Source: Towards Data Science - Walk-forward validation with expanding training windows and sequential testing periods

Best practices suggest reserving a final hold-out sample—perhaps the most recent 10-20% of available data—that remains completely untouched until after both traditional backtesting and walk-forward analysis. This ultimate out-of-sample test provides a final check against any inadvertent optimization of the testing process itself.

Cross-validation across multiple dimensions strengthens confidence further. Test strategies across different market conditions (trending versus ranging), time periods (bull and bear markets), and asset classes where applicable. A genuinely robust strategy should demonstrate consistent characteristics across these variations, not just within the specific dataset used for development.

Practical Implementation Guidelines for Trading Strategy Testing

Successful walk-forward implementation requires careful attention to configuration choices. For most systematic trading strategies, optimization windows should span 2-4 years of data, providing sufficient market history to identify meaningful patterns without extending so far that market structure fundamentally changes. Out-of-sample periods typically range from 3-6 months, balancing the need for meaningful validation with practical reoptimization frequency.

Key configuration decisions:

Optimization window size - 2-4 years provides adequate market history without structural changes

Validation period length - 3-6 months balances meaningful testing with realistic reoptimization frequency

In-sample/out-of-sample ratio - Common approaches use 70-80% for optimization, reserving 20-30% for validation

Window type - Rolling windows generally prove more realistic than anchored approaches

The right tools can significantly reduce the complexity of implementing these guidelines. Platforms that integrate both traditional backtesting and walk-forward analysis allow traders to start with rapid concept testing before graduating to more rigorous validation—without needing to master multiple software packages or write custom code. For investors who want to focus on strategy development rather than technical implementation, having these capabilities accessible in one environment removes significant friction from the validation process.

Transaction costs and slippage must be modeled realistically throughout all testing phases. Many strategies appear profitable in backtesting only to fail under realistic trading conditions once spreads, commissions, and market impact are properly accounted for. Conservative estimates prove wiser than optimistic assumptions—if a strategy can't survive pessimistic cost assumptions, it likely won't survive live markets.

Documentation best practices:

Track all iterations - Record each strategy version tested, not just successful ones

Log parameter ranges - Document all parameter combinations explored

Note validation outcomes - Keep detailed records of walk-forward results across all windows

Create audit trails - Build context for evaluating whether live performance deviates from expectations

Recording this development history helps prevent unconscious data mining and provides crucial context when evaluating whether subsequent live performance deviates meaningfully from expectations.

Beyond Backtesting: The Role of Forward Testing and Live Validation

Even the most rigorous historical validation cannot fully substitute for forward testing with real market data. Paper trading in live markets exposes strategies to execution challenges invisible in backtests: order fills at less favorable prices than expected, momentary illiquidity in supposedly liquid markets, and the psychological pressure of watching real positions move against you.

The graduated validation progression:

Historical backtesting - Quick concept validation and parameter exploration

Walk-forward analysis - Multi-regime robustness testing

Paper trading - Live market execution without capital risk

Small position live trading - Real capital deployment with limited exposure

Full deployment - Scaling to target position sizes after sustained success

This progression from backtesting through walk-forward analysis to paper trading and finally live trading with small position sizes creates graduated stages of validation. Each stage adds realism and reveals potential issues before they become expensive. The transition should be gradual, with strategies proving themselves at each level before advancing to the next.

Live validation also provides feedback impossible to obtain from historical data. Markets evolve, and a strategy's performance in current conditions may diverge from historical expectations for legitimate reasons rather than overfitting. Monitoring live results against walk-forward predictions helps distinguish between normal performance variation and fundamental strategy degradation requiring intervention.

The ultimate validation comes from sustained profitability across multiple market cycles. Strategies that remain profitable through different regimes—trending and ranging markets, high and low volatility environments, changing correlations between assets—demonstrate a robustness that no amount of historical testing can fully prove but that extended live experience can confirm.

Finding the Right Validation Approach for Your Trading Strategy

The choice between traditional backtesting and walk-forward analysis isn't binary—it's contextual. For traders developing momentum strategies with clearly defined parameters like moving average periods or breakout thresholds, walk-forward analysis provides substantial value by validating that parameter optimization truly improves out-of-sample performance rather than simply fitting historical noise.

When walk-forward analysis adds most value:

Parameter-rich strategies - Moving averages, oscillators, breakout thresholds benefit from iterative optimization

Complex systems - High-frequency strategies with dozens of parameters need rigorous overfitting protection

Machine learning models - Neural networks and ensemble models are highly susceptible to curve fitting

Systematic approaches - Algorithmic strategies with clearly optimizable numerical inputs

When traditional backtesting may suffice:

Fundamental strategies - Approaches based on economic relationships expected to persist

Pattern recognition - Discretionary methods without numerical parameters to optimize

Simple rule-based systems - Strategies with few parameters and clear, logical foundations

Market microstructure trading - Approaches exploiting structural market features

If a strategy lacks numerical parameters to optimize, or if its core logic derives from economic relationships expected to persist regardless of specific parameter values, traditional backtesting with proper data segregation may prove sufficient for validation.

Resource constraints once created a significant barrier to proper validation, but accessible platforms have democratized these capabilities. Individual traders who previously found comprehensive walk-forward analysis prohibitively expensive or technically complex now have access to tools that handle the computational heavy lifting. Whether you're testing a simple moving average crossover or a complex multi-factor model, having both backtesting and walk-forward validation available removes the technical barriers that once forced traders to choose between rigorous testing and practical feasibility.

The Evolving Landscape of Strategy Validation Methods

The field of strategy validation continues advancing beyond even walk-forward analysis. Recent research has introduced methods like Combinatorial Purged Cross-Validation that address some of walk-forward analysis's limitations, particularly its susceptibility to temporal variability and false discoveries. These sophisticated approaches create multiple training and testing combinations while respecting data chronology and preventing information leakage.

Machine learning's proliferation in trading has intensified focus on validation methodologies. Neural networks and ensemble models, with their thousands or millions of parameters, can overfit historical data with remarkable efficiency. This reality has driven development of specialized validation techniques incorporating penalties for model complexity and systematic approaches to avoiding the abundance of misleading results that plague machine learning applications in finance.

The democratization of computing power and data access means more traders can implement sophisticated validation techniques that were once the exclusive domain of institutional players. Modern platforms now provide accessible tools that handle the computational complexity of walk-forward analysis while offering traditional backtesting capabilities—making rigorous strategy validation available to traders at any experience level. These integrated solutions allow investors to test ideas quickly with traditional backtesting, then validate promising strategies through walk-forward analysis, all within a single environment that manages the technical implementation details.

The real breakthrough isn't just having access to these methodologies—it's removing the barriers that once made them impractical for individual investors. When strategy creation and testing tools become accessible regardless of technical expertise or resource constraints, more traders can focus on what matters: developing genuinely robust approaches rather than fighting with implementation complexity.

Yet technological advancement cannot eliminate the fundamental challenge: the future will differ from the past in ways impossible to fully anticipate. No validation methodology, however sophisticated, can guarantee future performance. The goal isn't certainty but confidence—developing strategies robust enough to adapt to reasonable market evolution while remaining grounded in genuine, repeatable patterns rather than transient noise. With the right combination of methodologies and accessible tools, traders at any level can build that confidence through rigorous, systematic validation.

Automate any portfolio using data-driven strategies made by top creators & professional investors. Turn any investment idea into an automated, testable, and sharable strategy.