Direct Indexing vs ETFs: Your Portfolio, Your Rules

Surmount Blogs

Direct indexing delivers 1-2% annual tax alpha through loss harvesting and full customization. Discover why it's replacing ETFs for taxable accounts.

For decades, the exchange-traded fund has been the default answer to a simple question: how do I invest in the market without picking individual stocks? With rock-bottom fees and instant diversification, ETFs democratized index investing for millions. They remain excellent instruments for what they're designed to do.

But they were never designed to do what many investors actually need:

They can't harvest your tax losses

They can't exclude the company your employer already pays you in stock options to own

They can't remove the oil companies or weapons manufacturers that conflict with your values

They can't adapt to the fact that you live in California and face a 13.3% state capital gains rate, not the 0% rate in Texas

Direct indexing can do all of these things. And the technology that once made this level of customization available only to families with nine-figure portfolios has now arrived for investors with a fraction of that. The shift is already underway—direct indexing assets closed 2024 at $864.3 billion, compared to $9.4 trillion in index-tracking ETFs. That gap is shrinking fast, with direct indexing assets having nearly doubled since 2021, representing a compounded annual growth rate of 22.4 percent.

The question isn't whether direct indexing will reshape how people invest. It's whether you'll be early or late to the change.

What Direct Indexing Actually Means

The concept is straightforward but often misunderstood. Direct indexing is an investment strategy that allows investors to purchase individual stocks that make up an index rather than buying a traditional index fund or exchange-traded fund. If you want S&P 500 exposure, instead of buying SPY, you buy shares of the roughly 500 companies that comprise the index—or a statistically representative subset of them.

This sounds like unnecessary complexity. Why own 500 stocks when you could own one ETF that holds them for you?

Because ownership matters. When you own an ETF, the fund company owns the stocks. You own shares of the fund. This seemingly minor distinction creates a wall between you and powerful tax and customization opportunities. When a stock inside your ETF falls 30%, you can't sell it to harvest that loss. The fund company might harvest it—but the benefit accrues to the fund, not to you personally. Your tax situation, your other investments, your specific timing needs—none of that enters the equation.

Direct indexing puts you on the other side of that wall:

You own the securities

You control when to recognize gains and losses

You decide which companies stay and which go

The Tax Efficiency Gap

Image Source: Russell Investments

ETFs already enjoy structural tax advantages over mutual funds. In 2024, just 5% of all ETFs distributed capital gains compared to 43% of mutual funds. Their in-kind creation and redemption mechanism shields investors from the taxable events that plague mutual fund holders.

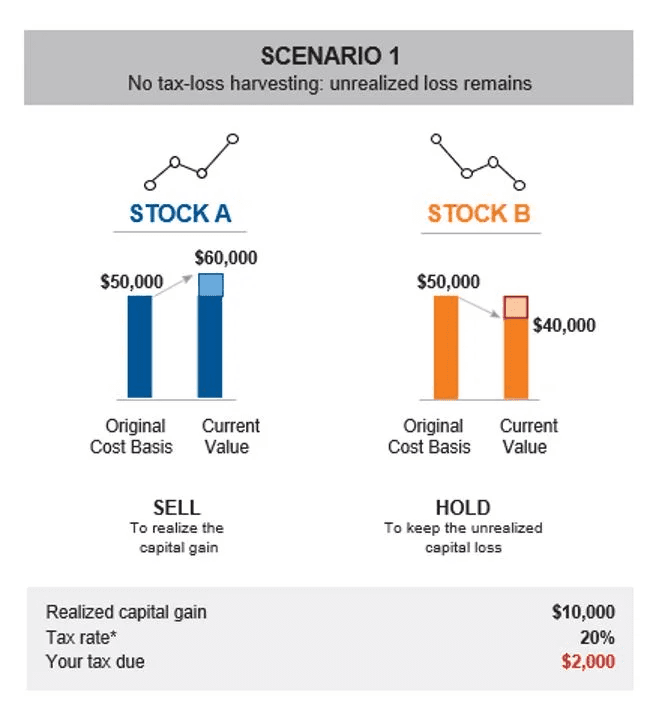

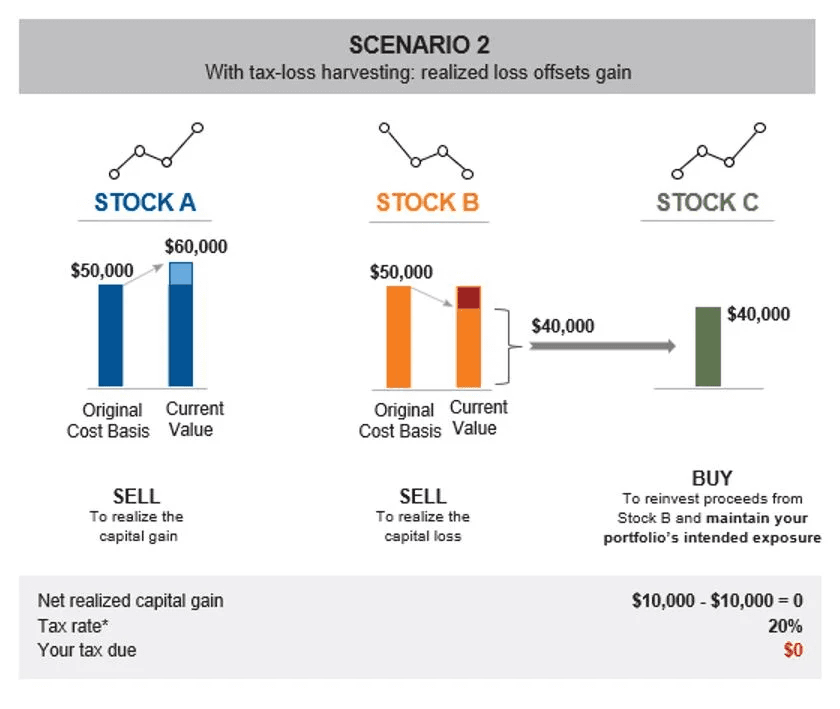

But ETFs still leave money on the table. The gains inside the fund that aren't distributed—they're just deferred, waiting to hit you when you sell. And the losses inside the fund? You never see those at all.

Direct indexing flips this dynamic. Routinely harvesting your losses can actually boost your after-tax returns relative to a traditional index over time. The value of taxes saved is sometimes called "tax alpha." Research from the Schwab Center for Financial Research quantifies this:

The S&P 500 Total Return Index averaged roughly 11% pre-tax return over the past 40 years

This results in an average after-tax return of about 8.38% (assuming a 23.8% long-term capital gains rate)

With tax-loss harvesting, that after-tax return rises to 9.41%

That 1.03 percentage point advantage compounds significantly over decades

The mechanism is intuitive once you see it. When loss harvesting is done at the market level using a broad market instrument such as an index ETF, harvesting losses would be much more difficult during strong bull markets. If investors owned component pieces of the market, however, they may be able to take advantage of stock dispersion and volatility. Even in 2023, when the S&P 500 rose 26.3%, approximately 170 stocks in the index ended the year with negative returns. That's 170 potential tax-loss harvesting opportunities invisible to ETF holders.

J.P. Morgan's research on daily versus monthly approaches to monitoring portfolios for tax-loss harvesting opportunities found that the daily approach provided, on average, about 30 basis points of additional annualized tax savings compared to monthly harvesting. The technology powering modern direct indexing platforms scans portfolios continuously, capturing opportunities that sporadic, calendar-driven approaches miss.

Customization Without Compromise

Tax efficiency attracts investors. Customization keeps them.

Values-based investing has moved from fringe to mainstream. 82% of respondents between the ages of 24 and 43 consider a company's ESG track record when making investment decisions, according to Bank of America's 2024 study of wealthy Americans. But ESG preferences are intensely personal. One investor wants to exclude fossil fuels; another wants to exclude weapons manufacturers; a third cares primarily about labor practices or board diversity.

ETFs respond to this demand with themed products—clean energy funds, socially responsible indexes, firearms-free portfolios. But these remain one-size-fits-all solutions to what are fundamentally individual problems. ESG is extremely subjective, and no pre-packaged fund can anticipate your particular hierarchy of concerns.

Direct indexing resolves this tension. Unlike conventional ESG funds that offer broad-based exposure, direct indexing offers a personalized approach that can precisely reflect an investor's ethical and sustainability values through custom screens and exclusions. Want to track the S&P 500 but remove gambling companies, add a tilt toward carbon-efficient firms, and exclude the three specific stocks your employer already compensates you with? That's a single portfolio, not a complex overlay of multiple funds.

Unlike an ETF or other commingled fund, direct indexing gives an investor greater control, allowing for tax-loss harvesting at the security level, customization around ESG preferences, and other advantages. The same technology that hunts for tax losses also rebalances the portfolio after exclusions, maintaining exposure profiles that track the benchmark while respecting your constraints.

The Democratization of Sophistication

Historically, direct indexing required substantial wealth—often $250,000 to $500,000 minimums, plus advisory fees that made it cost-prohibitive for anyone below the ultra-high-net-worth threshold. The strategy existed, but it was gated.

Three technological shifts have changed this:

Fractional shares: Commission-free trading and the advent of fractional shares lowered the minimum amount needed to construct the portfolio. You no longer need to buy full shares of Berkshire Hathaway at $700,000 each to include it in a direct index—fractional share trading allows precise allocation regardless of share price.

Automation: Advanced computer algorithms that automate the process replaced manual portfolio construction. What once required teams of analysts now runs on software that optimizes thousands of accounts simultaneously.

Competition: Competitive pressure from fintech platforms drove minimums down. Fidelity's Managed FidFolios launched with a $5,000 account minimum, twenty times lower than the firm's existing direct-indexing products. Other platforms have pushed even lower. Frec makes it easy for people to access direct indexing with a minimum investment of $20,000, while some platforms have arrived at the $5,000 threshold.

This isn't abstract democratization. It's the dismantling of a barrier that reserved tax alpha and customization for the wealthy. Tax-loss harvesting could generate an additional 1 to 2 percentage points of after-tax returns, depending on your situation. On a $50,000 portfolio over 25 years, that difference compounds into real money—money that previously flowed disproportionately to those who already had the most.

Where ETFs Still Win

Direct indexing isn't uniformly superior. Context determines which tool fits best.

Small accounts: ETF simplicity may still dominate. Managing hundreds of individual positions creates reporting complexity at tax time, even when brokerages provide consolidated 1099s. Some investors will prefer the cleanliness of owning one ticker.

International exposure: Direct indexing faces structural hurdles. ETFs composed of stocks from a single country lose their tax efficiency if local tax laws don't provide the same advantage for in-kind transactions. Direct indexing international equities also involves managing currency exposure and settlement across multiple markets.

Retirement accounts: For IRAs and 401(k)s, tax-loss harvesting provides no benefit—these accounts already defer or eliminate capital gains taxes. The customization advantages of direct indexing remain, but the primary tax alpha disappears.

Fee considerations: The fees for direct indexing typically run between 0.30% and 0.40%—as opposed to 0.20%, on average, for garden-variety ETFs and mutual funds. That fee differential needs to be offset by tax savings. For investors in low tax brackets without substantial gains to offset, the math may not pencil out.

The Generational Tailwind

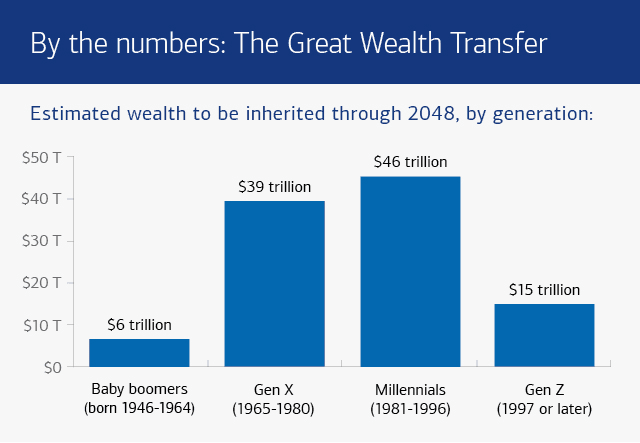

The largest wealth transfer in history is underway. Cerulli projects that wealth transferred through 2048 will total $124 trillion—$105 trillion is expected to flow to heirs, while $18 trillion will go to charity. The recipients are predominantly Gen X and millennials, and their investment preferences diverge sharply from their parents'.

With better access to retirement plans and digital investment platforms, millennials and Gen Z show different preferences—favoring self-direction, technology, and investing in a values-based direction. They've grown up customizing everything—playlists, news feeds, shopping experiences. They expect their portfolios to be equally personal.

85% of millennials and Gen Z prefer behavioral coaching from their advisors, highlighting a desire for more than just transactional financial advice. They want personalized, values-based guidance and expect their portfolios to align with their social and environmental values. ETFs—even the best of them—can't deliver this at the individual level.

The wealth transfer isn't just moving assets. It's moving expectations. And the tools that served Baby Boomers well may not serve their heirs at all.

Advisor Adoption Remains Low

Despite the structural advantages, advisor adoption remains surprisingly low:

Just 18 percent of advisors reported using direct indexing in 2024, a modest rise from 16 percent the year before

Roughly one-quarter (26 percent) said they had access to the strategy but opted not to use it

12 percent indicated they were unfamiliar with the concept

This creates asymmetry. The strategy is mature. The technology is accessible. The benefits are documented. Yet most advisors haven't adopted it, and most investors haven't experienced it.

Advisor education is crucial to adoption, as advisors are unlikely to recommend direct indexing strategies to their clients if they do not fully understand them. The gap represents opportunity—both for investors who adopt early and for platforms that make the transition frictionless.

Building Your Own Index

The rise of no-code and code-based investing platforms has further accelerated access to direct indexing. Investors no longer need to rely solely on traditional advisory relationships to construct customized portfolios.

Modern platforms allow you to define your index parameters—benchmark selection, exclusions, factor tilts, tax preferences—and then handle the execution, rebalancing, and harvesting automatically:

Some offer visual interfaces for investors who prefer to point and click

Others provide APIs for those who want to code their own rules and strategies

This is the logical endpoint of a trend that began with online brokerages and accelerated through robo-advisors: the progressive removal of friction between investor intent and portfolio execution. Direct indexing is the next layer, moving beyond "buy this fund" to "build this exposure, with these constraints, optimized for my tax situation."

Platforms like Surmount exemplify this evolution—enabling any investor to build their own direct index through either code or no-code tools. The sophistication that once required a family office now requires only a decision to use it.

The Path Forward

The debate between direct indexing and ETFs isn't really a debate. They're different tools for different contexts. The mistake is assuming that the tool you started with remains the right tool as your portfolio grows and your needs evolve.

Direct indexing provides structural advantages that ETFs cannot match for:

Taxable accounts with meaningful balances

Investors in higher tax brackets

Those with concentrated stock positions to manage

Anyone with strong values-based preferences

The math isn't even close—1% to 2% of annual tax alpha, compounded over an investment lifetime, materially changes outcomes.

The question to ask isn't whether direct indexing is better than ETFs in the abstract. It's whether the features that made ETFs revolutionary in 1993—simplicity, instant diversification, low cost—still represent your priorities today. For many investors, they don't. What matters now is:

Tax efficiency

Customization

Control

The platforms exist. The technology is proven. The minimums have fallen. The only remaining barrier is awareness—and that's disappearing too.

Automate any portfolio using data-driven strategies made by top creators & professional investors. Turn any investment idea into an automated, testable, and sharable strategy.