Finding Automated Investing Apps That Support Fractional Shares

Surmount Blogs

Discover the best automated investing apps that support fractional shares. Compare features, fees, and tax strategies to build a diversified portfolio with any budget.

The barriers to building wealth through equity markets have never been lower, yet many investors still overlook one of the most practical innovations in modern finance: fractional shares combined with automated portfolio management. This pairing has fundamentally altered who can access diversified investing and how efficiently portfolios can be managed, but understanding which platforms deliver both features effectively requires looking beyond marketing promises.

The Mechanics Behind Fractional Share Automation

Fractional shares allow investors to purchase portions of stocks and ETFs for as little as one dollar, fundamentally changing the calculus of portfolio construction. Rather than needing hundreds or thousands of dollars to buy a single share of companies like Amazon or Alphabet, investors can now allocate exact dollar amounts across multiple securities regardless of individual share prices.

When paired with automation, this becomes particularly powerful. The global robo-advisor market is projected to reach $2.38 trillion in assets under management by 2029, driven largely by investors seeking hands-off portfolio management that incorporates fractional trading. The combination allows for precise portfolio balancing that would be nearly impossible with whole shares alone.

Consider a simple example: an automated platform can maintain a target allocation of 60% stocks and 40% bonds by purchasing exact fractional amounts of ETFs, ensuring no cash sits idle and every dollar works according to your investment thesis. Without fractional shares, maintaining such precision would require significantly larger account balances or tolerance for portfolio drift.

Why Automation Matters More Than You Think

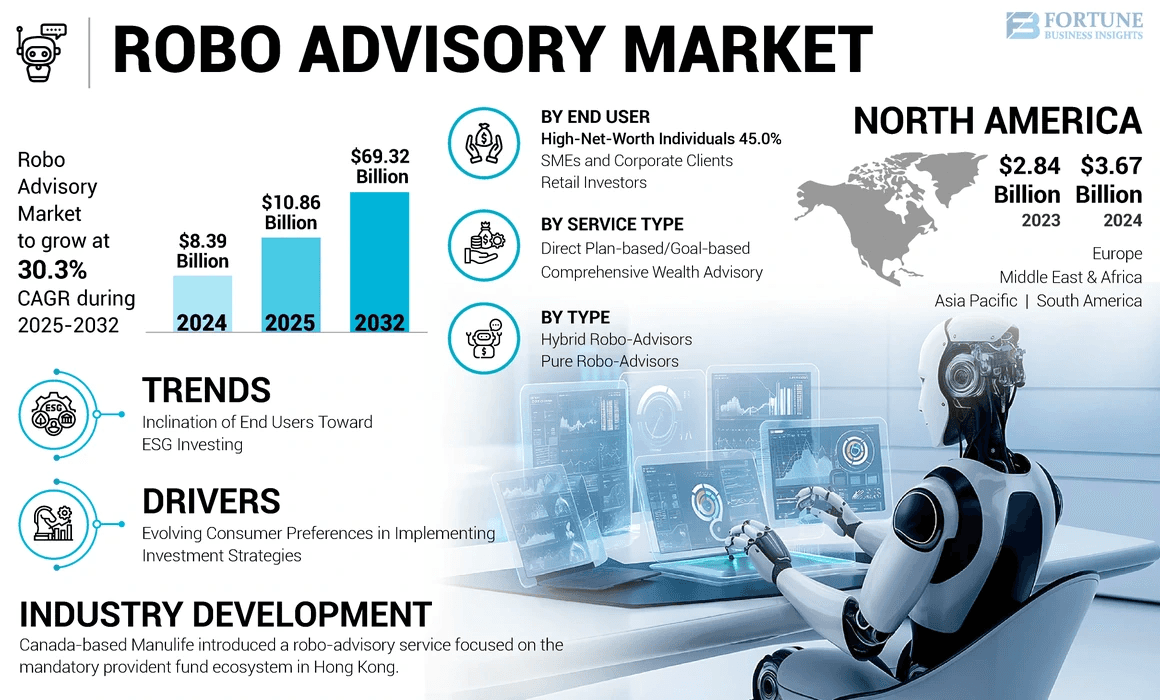

The value of automated investing extends well beyond convenience. Robo-advisory platforms have grown from $8.39 billion in 2024 to a projected $69.32 billion by 2032, reflecting both increased adoption and the tangible benefits these systems provide.

Modern robo-advisors handle several critical functions simultaneously:

Automated rebalancing as market movements cause drift from target allocations

Dividend reinvestment without manual intervention

Tax-loss harvesting strategies that meaningfully improve after-tax returns

Wealthfront estimates its clients have saved approximately one billion dollars in taxes over the past decade through automated tax-loss harvesting.

The behavioral advantages shouldn't be dismissed either. Automated systems remove emotional decision-making from routine portfolio management, keeping investors committed to their strategy during market volatility when manual intervention often produces suboptimal outcomes.

Platform Selection Requires Nuance

Not all automated investing platforms offer the same fractional share capabilities or automation features. The landscape divides roughly into three categories:

Traditional brokerages offering robo-advisor services

Pure-play robo-advisors

Hybrid models combining automated management with human advisor access

Platforms like Fidelity, Schwab, M1 Finance, and SoFi provide automated investing with fractional shares and customizable portfolios, but their implementation details vary significantly. Fidelity's approach emphasizes integration with their broader suite of investment products and research tools. Charles Schwab allows investors to buy fractional shares of S&P 500 companies for as little as five dollars each through Stock Slices, making their platform particularly accessible for investors focused on large-cap U.S. equities.

M1 Finance takes a different approach with its "Pie" portfolio system, allowing granular customization of automated portfolios using fractional shares across more than 80 ETFs. Their model appeals to investors who want algorithmic management but prefer to define their own asset allocation rather than selecting from preset risk-based portfolios.

The Tax Efficiency Dimension

For taxable accounts, the intersection of fractional shares and automated tax management creates opportunities that manual investing struggles to replicate. Wealthfront's daily tax-loss harvesting has generated an average annual harvesting yield of 4.23% across all portfolios over the past decade, demonstrating the compound value of systematic tax optimization.

Tax-loss harvesting works by selling securities that have declined in value to realize losses for tax purposes, then immediately reinvesting in similar securities to maintain market exposure. Key considerations include:

Schwab Intelligent Portfolios offers automated tax-loss harvesting for accounts with at least $50,000 in investable assets

Some platforms like Betterment and Wealthfront provide this feature at lower balance thresholds

The strategy can offset capital gains and up to $3,000 of ordinary income annually

The fractional share component becomes crucial here because it enables precise repositioning without leaving cash uninvested. When a platform sells a position at a loss and purchases a replacement security, fractional shares ensure the full proceeds maintain market exposure rather than sitting in cash waiting to accumulate enough for whole shares.

Diversification Without Scale

Perhaps the most democratizing aspect of automated fractional share investing is accessible diversification. Fractional shares allow investors to spread smaller amounts across different investments to help lower overall risk, enabling portfolio construction strategies previously available only to those with substantial capital.

An investor with $1,000 can now build a genuinely diversified portfolio across:

Multiple asset classes (stocks, bonds, real estate, commodities)

Different sectors (technology, healthcare, financials, consumer goods)

Various geographies (domestic and international markets)

Using automated rebalancing with fractional shares, that same investor maintains their target allocation as the portfolio grows through contributions and market appreciation, without needing to calculate how many shares of each holding to purchase.

This matters particularly for younger investors or those early in their wealth-building journey. Rather than concentrating capital in a handful of affordable stocks—a strategy that dramatically increases portfolio volatility—fractional automation enables proper diversification from day one.

Cost Structures Demand Scrutiny

The economics of automated fractional share investing vary considerably across platforms. Many platforms now offer commission-free trading with no account minimums, but this doesn't tell the complete story.

Common fee structures include:

Advisory fees as a percentage of assets (typically 0.25% to 0.50% annually)

Subscription models with flat monthly fees

"Free" platforms that generate revenue through payment for order flow

Required cash allocations that may create performance drag

For automated investors, the key consideration isn't any single fee in isolation but rather the total cost of ownership relative to value provided. A platform charging 0.25% annually but delivering tax-loss harvesting that saves 1% or more in taxes provides substantial net value. Conversely, a nominally "free" platform that requires holding 6% of the portfolio in low-yield cash may cost more than transparent fee alternatives.

Implementation Matters as Much as Features

The quality of automation varies significantly beneath surface-level feature lists. Robo-advisors use sophisticated algorithms to construct diversified portfolios and optimize asset allocation based on investors' risk profiles and financial goals, but the sophistication of these algorithms differs meaningfully.

Key implementation differences:

Some platforms rebalance only when portfolio drift exceeds predetermined thresholds

Others monitor daily for both rebalancing and tax-loss harvesting opportunities

The frequency and intelligence of these automated actions compound into material performance differences over time

Similarly, fractional share implementation matters. Some platforms allow fractional ownership of thousands of securities while others limit fractional trading to specific ETFs or stocks. The breadth of available investments directly impacts portfolio construction flexibility and the ability to implement particular investment strategies.

The Hybrid Model Gains Ground

Hybrid robo-advisory services accounted for 57.4% of market share in 2024, reflecting investor preference for platforms that combine algorithmic portfolio management with optional human advisor access. This model addresses a fundamental tension: investors appreciate automation's efficiency and objectivity but sometimes need human guidance for complex financial decisions.

Vanguard Personal Advisor Services exemplifies this approach, using automated portfolio management for routine tasks while providing access to human advisors for planning discussions and market questions. Schwab Intelligent Portfolios Premium charges a one-time planning fee of $300 and a $30 monthly advisory fee for unlimited guidance from certified financial planners.

For many investors, particularly those with more complex financial situations or those building significant wealth, this middle path offers optimal value. The automation handles portfolio management more efficiently than humans while avoiding the isolation some investors feel with purely algorithmic platforms.

Account Type Compatibility

The utility of automated fractional investing varies by account type. Tax-loss harvesting provides no benefit in tax-advantaged retirement accounts like IRAs, reducing the value proposition of sophisticated robo-advisors for those accounts. Some investors find simple target-date funds sufficient for retirement accounts while reserving automated fractional strategies for taxable investing.

Conversely, taxable accounts benefit tremendously from the combination of fractional precision and automated tax management. Russell Investments' 2024 research revealed portfolio rebalancing can help reduce portfolio volatility by as much as 1.2% over time, while simultaneously enabling tax optimization that enhances after-tax returns.

Account type considerations:

Taxable accounts: Maximum benefit from tax-loss harvesting and precise rebalancing

Traditional/Roth IRAs: Automation valuable primarily for rebalancing and discipline

401(k)s: Limited automation options, often better suited to target-date funds

Platform selection should account for which account types you're prioritizing. Some robo-advisors excel at taxable account management but offer limited retirement account features, while others provide comprehensive solutions across account types but with less sophisticated tax management.

The Rise of Direct Indexing

At the sophisticated end of automated investing, direct indexing combines fractional shares with individualized portfolio construction to enhance tax efficiency beyond what ETF-based portfolios can achieve. Rather than owning ETF shares, investors own fractional shares of the underlying individual securities, enabling security-level tax-loss harvesting.

Direct indexing advantages:

More frequent tax-loss harvesting opportunities

Individual security ownership rather than ETF wrappers

Customization capabilities (excluding specific companies or sectors)

Enhanced tax alpha through daily loss harvesting at the security level

While historically available only to high-net-worth investors, automated platforms are bringing direct indexing to broader audiences. The strategy generates more tax-loss harvesting opportunities by allowing losses to be harvested from individual securities within an index rather than requiring the entire ETF position to be at a loss.

This approach requires significantly more sophisticated portfolio management systems and typically higher account minimums, but represents the logical evolution of automated fractional investing for those who've accumulated sufficient assets.

Building Toward Financial Autonomy

The convergence of fractional shares and portfolio automation creates something more valuable than either feature alone: it enables evidence-based investing regardless of starting capital while removing behavioral obstacles that derail long-term wealth building.

Over 28% of Americans now prefer robo-advisor investing strategies, with adoption rates reaching 41% among millennials and 40% among Gen Z investors. This isn't surprising—these platforms make consistent, disciplined investing accessible without requiring constant attention or significant investment expertise.

Key selection criteria for your platform:

Your tax situation and primary account types

Desired level of portfolio customization

Preference for human advisor access

Minimum investment requirements

Fee structure alignment with your asset level

For investors seeking true automation with fractional capabilities, the platform choice matters less than ensuring alignment between the platform's strengths and your specific needs. Yet there's a critical gap most platforms haven't addressed: the ability to build and automate truly custom investment strategies without coding expertise or algorithmic complexity.

This is where platforms like Surmount are redefining what's possible. Rather than forcing investors to choose between preset portfolios or completely manual management, Surmount enables no-code strategy creation with institutional-grade automation. You can design precise allocation rules, implement sophisticated rebalancing logic, and automate tax-aware decisions—all while maintaining fractional share precision across your entire portfolio.

For advisors and sophisticated investors, this represents the natural evolution of automated investing: combining the accessibility and efficiency of robo-advisors with the customization previously available only through expensive discretionary management. The result is portfolio automation that adapts to your investment thesis rather than constraining you to someone else's.

The tools for intelligent, automated investing now exist at price points accessible to virtually anyone. The real question isn't whether to automate—it's whether to settle for pre-packaged solutions or demand a platform that truly understands how modern investors think about portfolio construction, tax efficiency, and long-term wealth building.

Automate any portfolio using data-driven strategies made by top creators & professional investors. Turn any investment idea into an automated, testable, and sharable strategy.