Practical Ways to Use AI to Improve Your Personal Finances

Surmount Blogs

Learn how AI budgeting tools, robo-advisors, and automated savings can improve everyday money decisions. Practical AI strategies for smarter personal finance in 2026.

Artificial intelligence has moved from science fiction to your bank account. What once required spreadsheets, financial advisors, and hours of manual tracking now happens automatically in the background of your financial life. But beyond the hype, how does AI actually help with everyday money decisions?

The answer lies not in replacing human judgment, but in eliminating the friction that keeps most people from making optimal financial choices. AI doesn't tell you what to value—it makes acting on those values dramatically easier.

Smart Budgeting: From Tracking to Predicting

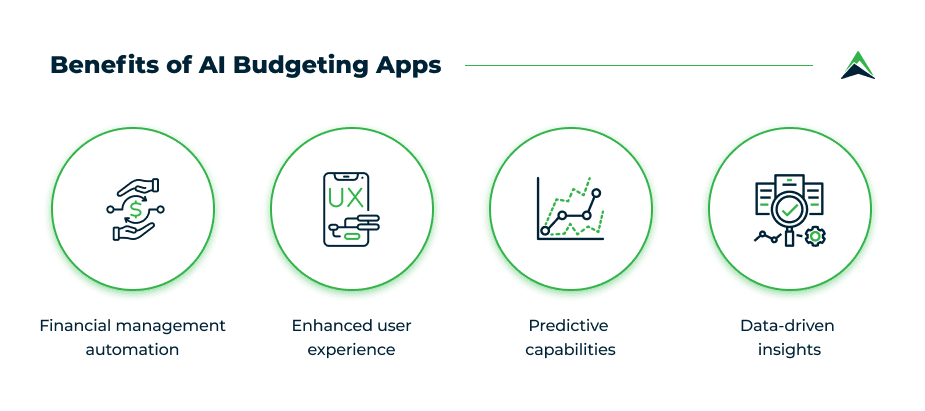

Traditional budgeting fails because it's backward-looking and labor-intensive. You categorize last month's spending, feel guilty about the results, and promise to do better next month. AI flips this model entirely.

Modern budgeting apps now predict your spending before it happens:

Forward-looking cash flow projections that show your likely account balance at month's end based on recurring bills and typical spending patterns

Automatic categorization of transactions without manual input, learning from your behavior over time

"Safe to spend" calculations that factor in upcoming bills, savings goals, and irregular expenses to show truly available funds

Anomaly detection that flags unusual spending patterns or potential fraudulent charges in real-time

Tools like Quicken Simplifi have overtaken older competitors by offering this forward-looking view. Instead of showing what you spent last month, they use AI to project your balance for the rest of the current month based on recurring bills and spending habits. It functions as a guardrail against overspending before it happens.

Automated Savings: Plugging the Leaks

Most people don't have a savings problem—they have a friction problem. When saving requires conscious effort and manual transfers, it competes with dozens of other priorities and usually loses.

AI removes that friction entirely:

Micro-transfer algorithms that move small amounts daily (from cents to $15) based on checking account activity, building savings invisibly

Round-up features that invest spare change from purchases automatically

Income-triggered transfers that detect deposits and immediately route a percentage to savings before you see it

Subscription detection that identifies recurring charges you may have forgotten, potentially saving hundreds annually

According to recent trends in personal finance automation, smarter automation can help plug hidden leaks like late fees, unused subscriptions, and idle cash. These aren't dramatic changes—they're invisible optimizations that compound over time.

Investment Management: Tax Optimization at Scale

Professional investors have long used sophisticated strategies to minimize taxes and maximize returns. AI democratizes these approaches for everyday investors.

What AI-powered investment platforms now deliver:

Daily tax-loss harvesting that captures micro-dips in individual holdings to generate tax deductions, happening far more frequently than any human advisor would execute

Direct indexing that allows you to own individual stocks rather than ETFs, enabling personalized tax strategies while maintaining diversification

Automated rebalancing that maintains target allocations without manual intervention or emotional decision-making

Fee analysis that scans linked accounts to uncover hidden mutual fund expenses, often revealing 1-2% in costs you didn't know about

The robo-advisor market is projected to reach $33.38 billion by 2030, driven largely by these capabilities. Platforms like Wealthfront lead in tax optimization, while Empower's AI-powered fee analyzer helps high-net-worth individuals identify costs that can erode hundreds of thousands over a lifetime.

The practical impact: strategies previously reserved for ultra-wealthy investors with teams of advisors become accessible at a fraction of the cost. Your portfolio works harder because tax drag decreases and hidden fees surface.

Fraud Protection: Catching Problems Before They Escalate

Traditional fraud detection relied on simple rules—charges over certain amounts or transactions in unexpected locations triggered alerts. AI analyzes patterns far more sophisticated than rule-based systems could manage.

Modern fraud protection includes:

Behavioral pattern recognition that learns your normal spending habits and flags deviations before you notice them

Biometric authentication that adds security layers without adding friction to legitimate access

Real-time transaction monitoring across linked accounts that spots coordinated attacks spanning multiple platforms

Predictive risk scoring that assesses transaction legitimacy based on hundreds of factors simultaneously

One report projects global losses from account takeover fraud rising from $13 billion to $17 billion in 2025 tied to increasingly sophisticated attacks. AI-driven security represents the primary defense against these evolving threats.

Financial Planning: Personalized Guidance Without the Advisor Fee

AI-powered planning tools analyze your complete financial picture and provide scenario-based guidance that adapts as your situation changes.

What this looks like in practice:

Goal-based planning that tracks progress toward multiple objectives simultaneously—retirement, home purchase, education funding—and suggests allocation adjustments

What-if modeling that shows the long-term impact of decisions like career changes, major purchases, or early retirement

Debt payoff optimization that calculates the most efficient repayment strategy across multiple obligations, factoring in interest rates and cash flow

Retirement projections that incorporate current savings, expected contributions, and market assumptions to estimate future income

By 2026, conversational AI, embedded finance, and biometric security are expected to be standard features in mainstream financial applications. This means asking natural-language questions and receiving personalized analysis becomes as common as checking your balance.

Investment Strategy Creation: Democratizing Quantitative Approaches

Perhaps the most significant development in AI-enabled finance is the ability for everyday investors to design and deploy sophisticated investment strategies without coding knowledge or institutional resources.

This represents a fundamental shift:

No-code strategy builders that allow you to test investment hypotheses using historical data

Backtesting capabilities that show how strategies would have performed across different market conditions

Automated execution that implements strategies consistently without emotional interference

Transparency into exactly why decisions are made, unlike traditional "black box" hedge fund approaches

Platforms like Surmount exemplify this democratization. By enabling both individual investors and financial advisors to create, test, and deploy automated investment strategies without programming expertise, they eliminate the traditional barrier between sophisticated quantitative approaches and practical implementation.

The practical impact: you're not limited to generic index funds or expensive active management. You can design strategies aligned with your specific goals, risk tolerance, and market views, then let automation handle execution.

Where AI Falls Short: The Human Element

For all its capabilities, AI has clear limitations that matter in personal finance:

Context ignorance: Algorithms don't know whether you value sustainable investing over maximum returns or understand the emotional weight of competing financial goals

Life complexity: When sudden illness strikes or job changes upend plans, AI lacks the wisdom to guide you through those human moments

Values alignment: Technology can't define what matters most in your financial life—only you can

As one financial advisor recently noted, AI doesn't know whether you value sustainable investing over maximum returns. It can't weigh the emotional complexity of saving for a child's education versus retiring early.

This is why the hybrid model now dominates successful platforms—combining AI's computational power with human judgment for complex decisions. Think of AI as a powerful calculator and your financial advisor as the mathematician who knows which equations to use.

Making AI Work for Your Finances

The key to benefiting from AI in personal finance isn't adopting every tool available—it's choosing capabilities that address your specific friction points.

Start with one or two high-impact areas:

If budgeting feels overwhelming, try an app with predictive spending and automatic categorization

If saving consistently is difficult, implement automated micro-transfers

If investment management seems complex, explore robo-advisors with tax optimization

If you want more control over strategy, investigate platforms enabling custom approach design

The broader principle: AI's value lies in automating what should be automatic and surfacing insights that inform better decisions. It doesn't replace judgment—it eliminates the tedious work that prevents most people from exercising good judgment consistently.

For investors seeking to build long-term wealth, AI-enabled tools represent not a replacement for human wisdom but an amplification of it. The most successful approach combines algorithmic efficiency with human values, letting technology handle execution while you focus on what truly matters in your financial life.

Automate any portfolio using data-driven strategies made by top creators & professional investors. Turn any investment idea into an automated, testable, and sharable strategy.